WPA Health Insurance Review (Extensive Guide 2022)

WPA is a not-for-profit health insurance specialist

About WPA

WPA is a not-for-profit company; they don’t have shareholders, which means they are free to reinvest profits back into the business and its members. Secondly, WPA is a specialist health insurer; it’s all they do, so they can focus their energy and resources on providing the best products possible.

Like many in the market, WPA promises a flexible approach to health insurance, giving you many options to customise your cover. Finally, WPA sets out to consistently provide transparent, open and honest services, and as we’ll go on to explain, their customers think they deliver on this promise.

Core benefits of WPA health insurance

In this review, we’ve focused on WPA’s two flagship policies, Flexible Health: Premier and Flexible Health: Elite, both of which can be described as comprehensive.

Here are the top benefits of both their Premier and Elite policies:

Inpatient and day-patient treatment in almost any private hospital in the UKAccess to any consultant or specialist in the UK (within reasonable cost limits)Complex diagnostic scans such as MRI, CT and PET are includedAccess to drugs that may not be available via the NHSTherapies and dental cover included as standard with the addition of optional outpatient coverExcellent cancer care, if you opt for their Elite policy or take out Cancer Care alongside your Premier policyShared responsibility excess, which reduces the amount you contribute towards each claimOutpatient cover is included in both plans, although with a relatively modest limit (£350) with their Premier plan

Unrestricted consultant choice, excellent hospital list and a fair approach to claims

As we’ll explain later in this review, several things stand out against most of the other leading health insurers. Namely, they give you unfettered access to any consultant in the UK. You also get access to nearly every private hospital, the only exclusions being high-end HCA hospitals (although these can be included for an increase in your premium).

The other thing to note is that WPA operates what’s known as a “community-rated scheme”, which simply means that your individual claims won’t affect your premiums. The collective claims of all of their members will be factored into your renewal premiums; thus, it is “community-rated”. WPA are one of only a few health insurers to offer this, and it basically means they won’t increase your premium if you make a claim.

Brilliant from start to finish.

Peter Ernes

on Google

Compare Policies

Disadvantages of WPA health insurance

There’s only one disadvantage that we think is worth mentioning: WPA doesn’t offer cover for people who are over 65-years-old.

WPA Premier vs Elite plans

WPA’s two best health insurance policies are Flexible Health: Premier and Elite, and while they share many similarities, there are some differences to bear in mind. Premier is WPA’s mid-range policy, whilst Elite offers more comprehensive cover.

Both policies have optional extras you can choose from and several co-payment levels, which is WPA’s equivalent to a standard excess.

Whichever policy you choose, you’ll receive cover for inpatient and day-patient treatment, including medicines and even prosthetic limbs, with no annual benefit limit.

WPA’s Cancer Cover

Flexible Health: Elite includes extensive cancer treatment and care as standard; however, to benefit from cancer care with a Premier plan, you’ll need to take it out as an additional extra. Whichever way you choose to buy it, you’ll find that WPA’s Cancer Cover is excellent.

Their Elite plan and the optional Cancer Cover attached to a Premier plan cover you for initial diagnosis, including consultations with a specialist and second opinions if necessary. They also cover diagnostic tests, scans and biopsies.

Cover is available for treatments including surgery, radiotherapy, chemotherapy and other targeted therapies as long as they are provided as a potential cure.

The NHS cash benefit is also included in the Elite plan, with cashback available for outpatient cancer treatment and restorative dental work following oral cancer.

Does WPA provide outpatient cover?

With both the Premier and Elite plans, you’ll have Outpatient Cover, although it has to be said the combined limit of £350 on the Premier plan is relatively modest. You can, of course, choose to upgrade that if you wish, up to either a £1,000 or £1,500 annual limit.

WPA’s Outpatient Cover includes all of the following:

Consultations with a specialist and diagnostic testsGP referred diagnostic tests (most insurers require you to see a specialist first)Therapies such as Physiotherapy and Osteopathy (limits apply)Complex diagnostic scansGP referred complex diagnostic scans (one MRI or CT scan)Outpatient proceduresPre-admission tests

Whether you choose their Elite Plan or Premier plus additional outpatient cover, you’ll have up to 10 sessions of GP referred therapy, such as physiotherapy, osteopathy chiropractic treatment. You’ll also be able to self-refer for up to four sessions of the same.

As we highlighted above, WPA will cover the cost of GP Referred Diagnostic tests, which is almost unheard of with other insurers. Yes, limits apply, but still, the fact you can see your GP and be directly referred for private diagnosis and even complex diagnostic tests is excellent.

Finally, and as we’ll explain in the next section if you opt for either their Elite plan or Premier with either £1,000 or £1,500 of outpatient cover, they include Dental and Optical cover.

Dental and Optical Cover

Dental and Optical Cover is included as standard with WPA’s Elite plan, and if you add extra Outpatient Cover to your Premier Plan, you’ll get it too, albeit a little more limited in coverage. With Elite, you get up to £450 towards General Dental Treatment, £250 for Dental Emergencies and £20,000 for Dental Injuries. If you opt for a Premier plan with an upgraded Outpatient Cover, you’ll just get £200 towards General Dental Treatment.

When it comes to Optical Cover, you get the same whether you opt for their Elite plan or Premier plus additional outpatient, in £200 per year towards Optical Treatment. This includes cover for sight tests, prescribed glasses, contact lenses and safety spectacles. The only stipulation in this respect is that all frames, lenses and contacts must be purchased in the UK.

WPA’s Mental Health Cover

Until relatively recently, WPA didn’t offer any Mental Health Cover. However, you can now add it as an optional extra to both their Premier and Elite policies. With the “Mental Health Treatment” option, you’ll have cover for 28 days/nights of inpatient and day-patient treatment. They’ll cover you for up to £1,000 in outpatient mental health treatment, such as consultations with a psychiatrist, psychotherapist or psychologist. Finally, you’ll have access to up to 20 structured counselling sessions per year as long as you are 16 or older if you opt for this extra.

Even without the optional extra, you’ll still have some mental health support in a health and wellbeing helpline. You can self-refer for a single telephone counselling session and online computerised Cognitive Behaviour Therapy (CBT). If you’re over 16, the helpline can also refer you for up to six structured counselling sessions.

Compare WPA To Other Leading Providers

Compare the UK’s leading health insurance providers and save up to 37% on your policy.

Compare Policies

on

Virtual GP service

The pandemic has surprisingly led to a reduction in waiting times for NHS GPs. As highlighted in this report, you can still expect to wait on average 8.7 days for a non-urgent, in-person appointment, and that’s after you’ve had an initial phone or video consultation. Before Covid, health insurers were already providing virtual GP services, and their popularity has only increased as more people look to limit close contact. The most attractive thing about virtual GPs is that they are available 24/7, 365 days a year, allowing patients to seek medical advice on a schedule to suit them.

Unlimited Virtual GP access

With both WPA’s Premier and Elite health insurance, you can access their Remote GP Service. You can have unlimited telephone calls and video consultations with fully qualified and practising doctors. Like a traditional GP, a private GP can prescribe medications, diagnose illnesses, and refer you to a specialist.

Other benefits and optional extras

As noted later in some first-hand customer reviews of WPA, their approach policies and approach to claims and customer services look to ease the pressure during difficult times. Their added benefits include access to services that make potentially stressful medical treatment slightly easier.

WPA’s Premier and Elite policies both all of these:

Up to 4 weeks nursing at homeTransport by private ambulanceUp to 10 nights’ hospital accommodation for a parent to stay with a child£10 per day for out of pocket expensesUp to £700 (£70 per day or night) donation to a hospiceNHS Cash Benefit

In addition, their Elite policy also includes:

Up to £200 for health screeningUp to £500,000 for emergency treatment overseas (although this doesn’t include the USA or its overseas territories)

What does WPA exclude?

As with any health insurance, there are some standard exclusions, alongside some more specific ones. For a complete list, please see later in this review where we share WPA’s policy guides, detailing their exclusions in full. These are their standard exclusions:

Pre-existing conditionsLong term chronic conditionsFertility issues, pregnancy and childbirthAllergic conditionsInjuries sustained through dangerous sportsAny treatments not approved by NICE or drugs used outside of their licensed indicationEmergency treatmentBreast surgery (unless following cancer surgery under the Cancer Care benefit)Cosmetic and aesthetic treatmentsAny form of cosmetic dentistryDeliberately self-inflicted injuries or attempted suicideEnd of life careHIV, AIDS

It has to be said that these exclusions are in line with the rest of the market, so there is no need for concern. If you want to know more specifics, please refer to the policy documentation later in this article, or request a comparison quote, and our brokers can answer your questions when you speak.

WPA have one of the best hospitals lists on the market

WPA prides itself on offering customers access to a wide range of hospitals and other treatment centres. Their extensive hospital list includes both NHS and private hospitals across the UK and specialist clinics and scanning centres.

The only exception they make is some of the most prestigious private hospitals in Central London, operated by HCA. However, if you would like those hospitals included, you can pay an increased premium to have them on your list.

Via WPA’s website, you can search for private healthcare facilities and quickly find those local to you.

Unrestricted consultant choice

WPA’s approach to individual consultants is consistent with its’ policy on hospital choice, and you have near free reign over who provides your treatment. While there are limits on the cost of procedures (all insurers have these), you can use them if your consultant doesn’t exceed those limits.

WPA’s ethos when it comes to consultant choice is that they believe their customers should be able to choose their treatment provider based on clinical need rather than on a commercial basis.

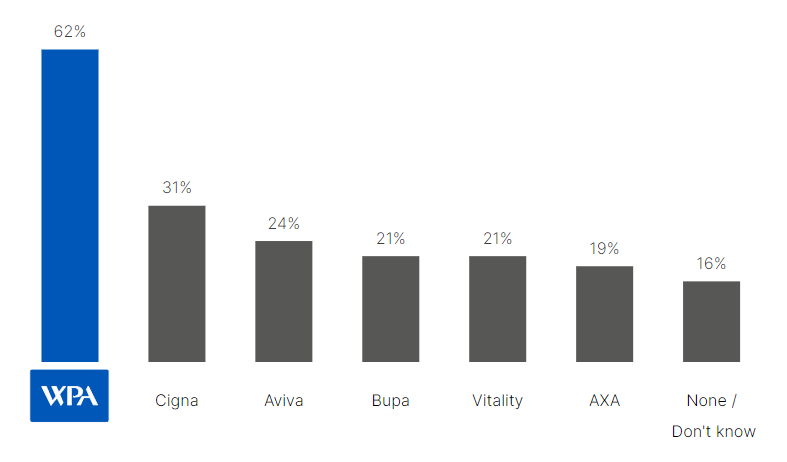

Not only do you get free reign to consultants, but by in large, those performing your treatment rate WPA as the easiest to deal with as they give them the freedom to exercise their clinical judgement. In this recent Populus study, 62% of consultants commended WPA, with their closest rival, Cigna, scoring 31%.

62% of consultants commend WPA

In a recent Populus survey 62% of consultants commended WPA

In a recent Populus survey 62% of consultants commended WPA

Underwriting options

When it comes to underwriting, you have a few options with WPA health insurance:

Moratorium – you won’t need to share your medical history, but any conditions you’ve had symptoms, treatment or advice for in the preceding five years will be excluded. However, if you have no symptoms, medication, or treatment for two years after joining WPA relating to those conditions, they will be covered there.Full Medical Underwriting – with this type of underwriting, WPA will review your past medical history, and in most cases, recent or ongoing medical conditions will be excluded. Switch – this is for those transferring from another insurer to minimise exclusions.

Unlike many of the other leading health insurance providers, WPA won’t change the price of your plan based on the form of underwriting you choose.

WPA’s shared responsibility excess explained

WPA doesn’t offer a traditional excess on their policies; instead, they offer a “shared responsibility excess”, which operates as a co-payment system. Under this system, you’ll contribute 25% of the value of your claim, up to a limit you choose, and WPA will cover the rest of the bill.

The higher you set your shared responsibility excess, the lower your premiums will be, so if you have some savings and can afford to contribute a reasonable amount to claims, it might be worth considering as it can bring the price down significantly.

The benefit of this relatively unique approach is that you’ll only pay a small contribution for more minor claims. So, for example, if you had a £250 co-payment limit and saw a specialist at a total cost of £175, you’d pay £43.75, and WPA would cover the rest. Compare that to a £250 traditional excess with another provider, and you’d have to pay all of it!

Does WPA offer any discounts?

WPA offers discounts of up to 20% for self-employed and professional workers and preferential terms for families compared to the cost of individual policies.

Self-employed and professional discounts

WPA’s discounts for the self-employed and other professionals give you up to 20% off of your premium until you’re 55, after which it reduces by 2% per annum up to the age of 65. Also worth noting is that the discounts apply to policyholders’ family members too!

WPA has a list of eligible professions on their website, so if you’d like to know if you can benefit from this discount, check here.

Multi-family healthcare

Discounts are also available on WPA’s multi-family healthcare plan, which provides cover for two or more families living at different UK addresses. This means that a single policy can provide cover for an extended family and includes a multi-family discount which reduces the cost per person compared to a single health insurance policy.

WPA customer reviews

While the features and benefits of any health insurance policy will be a critical factor in your choice of provider, customer reviews will give you a clear picture of the kind of service you can expect. WPA collect customer reviews via Trustpilot, where they currently enjoy an outstanding score of 4.7 out of 5 from over 1,000 reviews. Among the positive reviews are frequent comments about the excellent customer service, clear communication and a quick and straightforward approach to claims payment. Several reviewers mention WPA’s superb app, which simplifies claims, but they also point out that they’re always on the end of the phone if necessary. One reviewer describes WPA’s service as ‘taking the pressure off at a stressful time‘. There are a handful of negative reviews from customers who’ve experienced slow service or where claims have been declined, often because of misunderstandings around cover limits. However, as is demonstrated by the higher overall score, these negative reviews are relatively few and far between.

How much does WPA Health Insurance cost?

In February 2022, we got quotes for WPA Premier Health Insurance for several ages in ten cities around the UK. We included £1,000 of outpatient cover (which includes therapies, dental and optical cover). We chose moratorium underwriting and didn’t include mental health cover. We only got quotes up to 60-years old, as WPA’s cover stops at 65. The prices shown are averages based on 10 locations in the UK. Please note the price you pay will be different, and you should always get a comparison quote and speak to a broker before making a decision.

Age

Average price

20-year-old

£36.60

30-year-old

£44.94

40-year-old

£59.17

50-year-old

£74.94

60-year-old

£111.38

Our rating and summary

Overall we think that WPA’s health insurance along with the customer service and approach to claims is one of if not the best available in the UK today. While they’ll only provide cover until you’re 65, they’re a great option for anyone younger than that. Our expert rating is 4.7 out of 5, the highest score we’ve given any health insurer this year.

We hope that this has been a useful review of WPA health insurance. To sum up, here’s what you can expect from WPA:

Flexible health insurance policiesExcellent customer service (according to their reviews)Quick and straightforward payments (also according to their reviews)Cover for inpatient, day-patient and outpatient treatment as standardAccess to a virtual GP as well as health and wellbeing supportAccess to the NHS hospital cash benefit if you need to stay in hospitalA range of optional extras.Cover for cancer treatment, dental care and optical care as standard on the Elite plan.An alternative to the standard health insurance excess with the shared responsibility excess.Access to over 600 hospitals and treatment providers.Discounts for self-employed people, professionals and extended families.

More information

If you’d like to know more about WPA Flexible Health Premier and Elite please click on the PDF links below to download their policy documentation.