Why You Can’t Trust Online Quotes for Mortgage Protection (even ours)

I know what you’re thinking – Is this fella trying to turn away my business?

Obviously, that’s a big fat nope. I love helping you guys get the best bang for your mortgage protection buck, but I’m also going to be brutally honest so that you can get the best deal.

I’m doing this by shouting from the rooftops not to trust any online quote for your mortgage protection, even the quotes you may have got from my online quote predictor.

But why!? I hear you cry.

Why you shouldn’t trust online quote engines

There are a lot of factors that go into your final quote. You know, the one you sign on the dotted line for. Online quote systems just don’t take into account every little piece of info that can turn that lovely low premium into a monster monthly outlay.

You see those online quotes assume you are in perfect health.

No history of family illnesses, normal BMI, fit as a fiddle.

But once you apply for that quote and start on your application form, you’ll quickly realise on thing:

Those insurance lot are a bunch of truly nosey buggers and want to know things you never even considered when you were tapping away and getting a quote.

Look, if you’re in perfect health, the ideal weight, only take a small sherry on special occasions, and have a family that is entirely free of any sort of illnesses it may be possible that your online quote is correct but that’s how they reel you in.

Really, what I’m telling you is ‘Don’t fall for the cheapest quote that falls into your lap’ trap.

The saying ‘it’s too good to be true’ is one that should come as a disclaimer for most of these quick and easy quotes you snag from an insurance website.

Still think I’m telling porky pies, that’s cool, I can appreciate a cautious shopper.

Let me tell you a story.

Why the price you see may not be the price you pay

Sarah got a mega cheap quote for her mortgage protection insurance from a big insurer we shall not name (No, it’s not Voldemort, although if you want to imagine it is, well you do, you boo)

So, what did she do next? She got a little call back from a rather friendly salesperson, and she decided to proceed.

A medical questionnaire arrived in her inbox within minutes, asking questions her mother wouldn’t have the cheek to ask.

Sarah’s BMI was just a smidge over the ‘healthy range’, so the provider added a good deal extra to her initial quote. She also has mild IBD, so you can guess what happened next.

Yup, you got it! More money on her monthly for the insurer.

She also has Type 1 Diabetes; a long-term chronic condition diagnosed when she was only three. Even though it’s a condition outside her control, she has to pay more because the insurers see her as a bigger risk.

By now, that cheap quote is nothing but a mere memory. Instead, she’s faced with a premium so far from her expected budget that angels begin weeping.

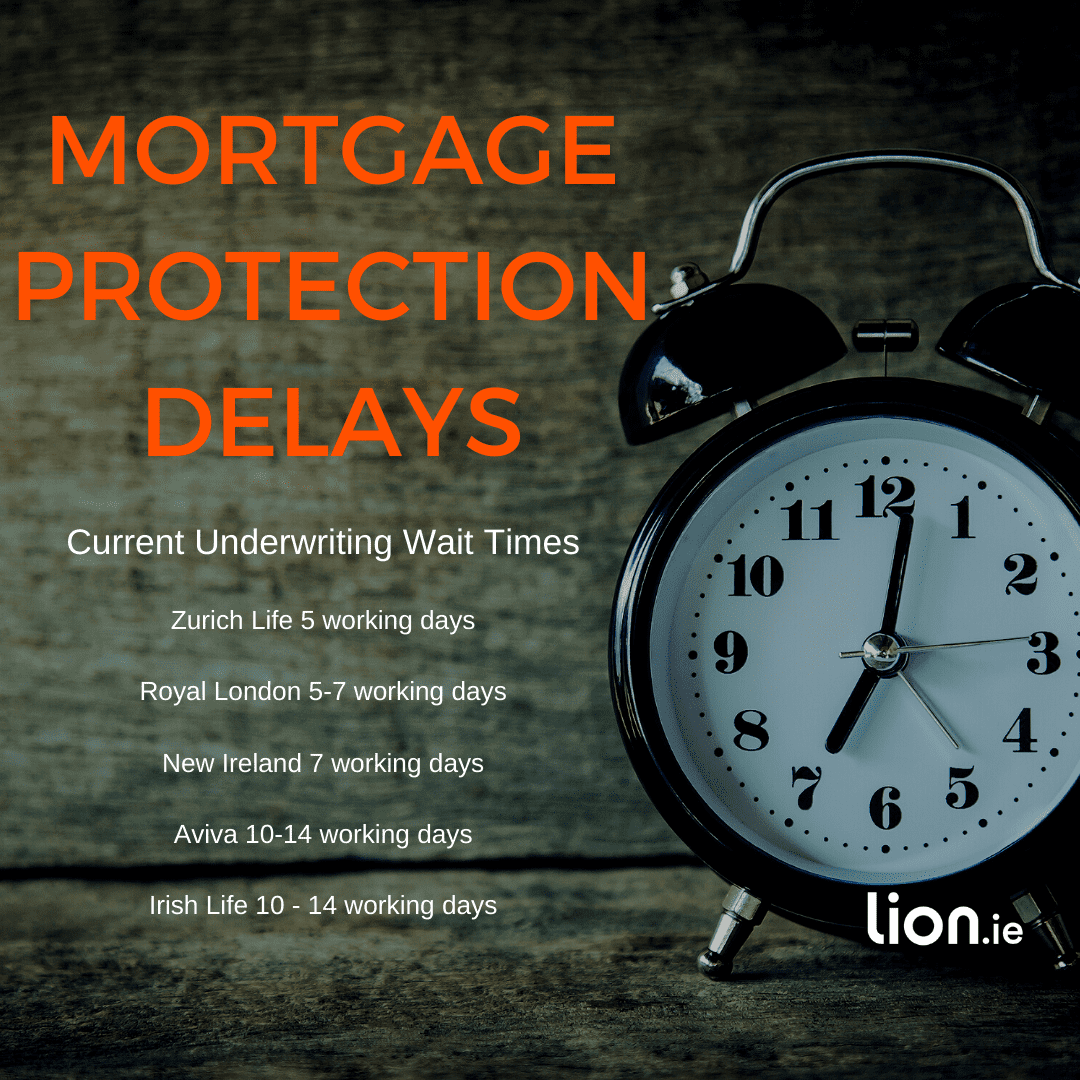

Even worse, the underwriting process took so long that she had no time to turn around and say goodbye when she got the big fat bill.

Sarah made the fatal mistake of trusting that super cheap online quote and got stuck with a premium she could barely afford.

It sounds mental, but honestly, you would be surprised how often this actually happens.

So, what should you do?

How to get a better mortgage protection quote?

Research, research, research.

Yeah, it seems old school, but sometimes the old ways are the best. Get that phone out and ring around. Ask all the nitty-gritty questions you need to and don’t agree to any old plan because you have a hard time saying no.

Another piece of advice I have is that specialist life insurance advisors can be your best pal when navigating the wilds of the mortgage protection world. It’s our job to get you the best deal. That saves you a whacking great deal of time because we do all the heavy lifting for you.

Look, if you have a chronic medical condition like MS, Diabetes, IBD, your weight isn’t the best, or you love a sneaky cig with your morning coffee, you’re always going to pay a little extra than neighbour Ned, but that doesn’t mean you can’t shop around and find a better dealio.

Insurance companies are businesses. They are trying to attract as many customers as they can that fit their “risk profile”, so just because your face doesn’t fit with Insurer A, give Insurer B a try.

And look, just because you’ve signed on the dotted line and are paying through the nose doesn’t mean you can’t look elsewhere.

Your current insurer can’t put a gun to your head and demand you stay with them, although if they could get away with it…

*Disclaimer* Threats of violence or torture to ensure they keep your business are, in fact, illegal and nothing you should actually be concerned about.

What to do next?

So, do you feel a little more at ease now that I’ve explained why you can’t trust me, or at least my online quote?

See, I’m not a bad guy after all.

Now here’s my little bit of self-advertisement

I want you to get the best deal because that’s what you want, right?

You don’t want to spend three days on the phone ringing around every insurance provider under the sun.

That’s cool, I can dig.

Perhaps, all the mumbo jumbo language has your head spinning.

I’ve got you. I understand all that and can talk you through it.

Or maybe you just want to see if there’s a better mortgage protection provider out there for you.

I’ve got your back. If they’re there, I’ll find them.

Schedule a callback here, or complete this questionnaire and let’s see what magic I can muster for you.

Thanks for reading

Nick