Why Personal Auto Insurance RatesAre Likely to Keep Rising

Personal auto insurance premium rates have returned to pre-pandemic levels, but several trends are likely to sustain upward pressure on rates, according to a new Triple-I Issues Brief.

At the start of the pandemic, auto insurers – anticipating fewer accidents amid the economic lockdown – gave back approximately $14 billion to policyholders in the form of cash refunds and account credits. But while miles driven declined and accident frequency initially dropped, frequency and severity quickly started increasing again. Traffic fatalities also increased, after decades of steady declines.

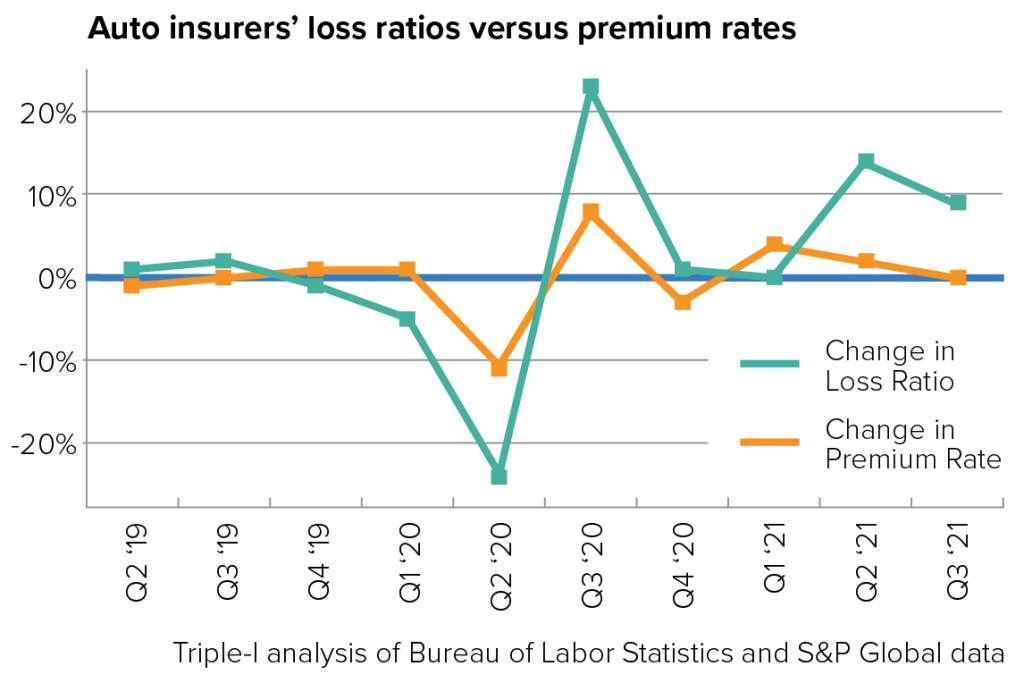

While insurers’ personal auto loss ratios fell briefly and sharply in 2020, they have since climbed steadily to exceed pre-pandemic levels. With more drivers on the road and replacement parts climbing, this loss trend is expected to continue.

Auto premium rates reflect a range of factors that contribute to an insurer’s loss experience. In a world of perfect information, rate changes would correlate perfectly with changes in loss experience. As the chart below shows, until the pandemic these two metrics for the overall industry tracked quite closely. The disruptions of 2020 led to volatility for both, and losses have proved more volatile than pricing.

Barely profitable

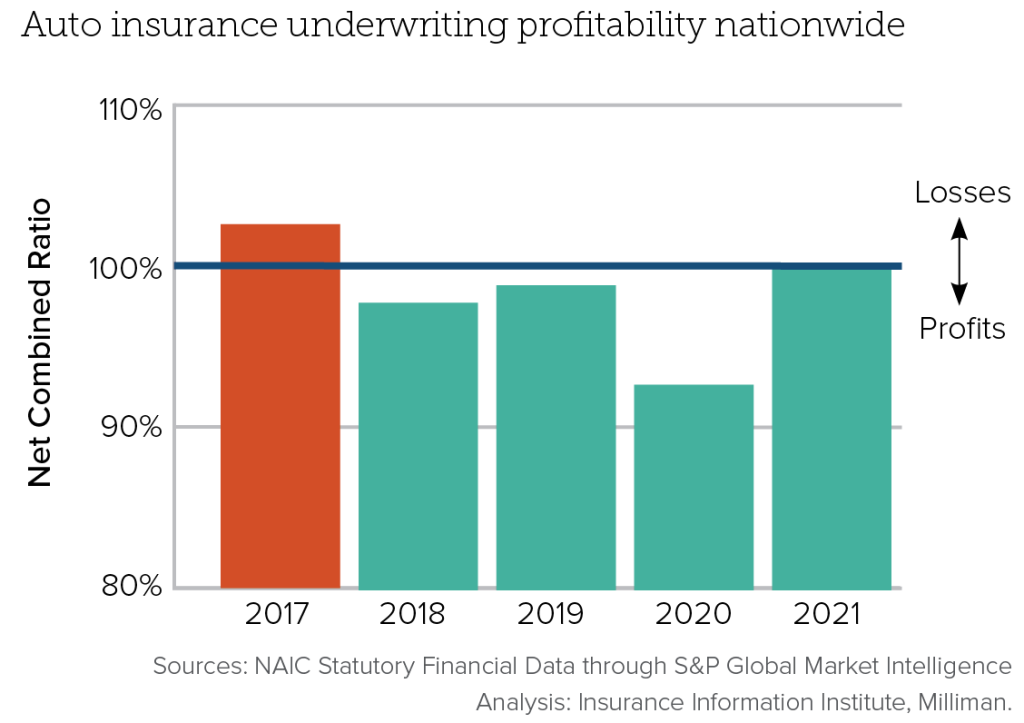

To remain viable, insurers have to set premiums at levels appropriate to the risks they cover. Insurers’ underwriting profitability is measured by a “combined ratio”, which is calculated by dividing the sum of claim-related losses and all expenses by earned premium. A combined ratio under 100 percent indicates a profit. A ratio above 100 percent indicates a loss.

As the chart above shows, personal auto insurance has been a barely profitable line for the industry for years. If recent accident and replacement-cost trends persist, upward pressure on premium rates is likely to continue.

Learn More

Facts + Statistics: Auto insurance

Why Did My Auto Insurance Costs Go Up Even When I Didn’t File a Claim?

Triple-I Offers U.S. Insights into Auto Insurer Pricing Factors