What is a novated lease on a car and what do I need to know before signing up?

If you’re thinking about getting a vehicle but don’t have enough money saved, you might be considering a choice between taking out a car loan or a novated lease (also known as “salary sacrificing” to get a car).

It’s important to know the difference, as there are plenty of tax implications and what’s right for one person won’t be for another.

So, what is a novated lease and how does it work?

Ever thought of taking out a novated lease on a car?

Photo by Lisa Fotios/Pexels, CC BY

A novated lease involves your employer

Under a normal lease, you enter an agreement with a leasing company. They buy the vehicle you’ve chosen (and own it until the end of the lease) and you get to use it in return for making regular lease payments. At the end of the lease agreement period, you can choose to make an additional payment (called a residual or balloon payment) and take over ownership of the vehicle.

A novated lease includes another party in the agreement – your employer.

In this case, your employer makes the payments to the leasing company on your behalf, then reduces your wages by the amount of the payment.

This is called a salary sacrifice or salary packaging arrangement and it means you end up paying less tax on your income.

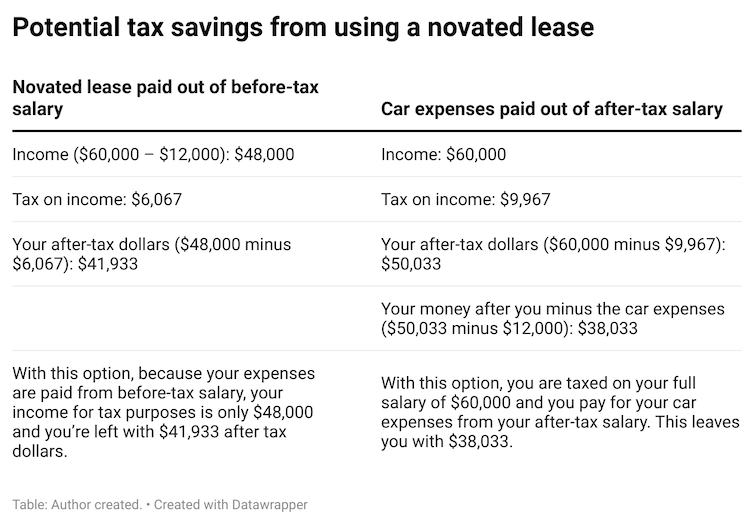

To demonstrate the tax saving, see the example below, which is based on a vehicle expense of A$12,000 for the 2022-23 tax year.

Potential tax savings from using a novated lease.

Bundled with the novated lease is the finance or interest component, at a rate similar to a car loan. However, it is easier to obtain finance through a novated lease as your employer is guaranteeing the payment out of your salary.

Used or new car? What about running costs?

You can purchase a new or used vehicle under a novated lease.

Also, you may be able to bundle not only the purchase price and the finance costs, but also the running costs such as fuel, servicing and insurance.

This means the total costs of owning a vehicle are bundled into a single payment and deducted from your before-tax salary. This is called a fully maintained novated lease.

How does it compare with a traditional car loan?

A traditional loan involves borrowing money from a lender (such as a bank) to pay for your vehicle.

You become the owner of the vehicle straight away, but you have a debt (which is usually secured against the vehicle itself). You’ll need to make regular loan repayments plus interest.

If something goes wrong and you can’t make your regular repayments, you may be forced to sell the vehicle to cover the debt.

You’re also directly responsible for all the running costs, which you pay from your after-tax salary.

Since you own the vehicle, you may be able to claim some tax deductions if you use it for work.

Make sure you understand what you’re signing up for.

Photo by Antoni Shkraba/Pexels, CC BY

5 things to think about before you sign up for a novated lease

Check if the novated lease arrangement is tax effective for you. There may be other costs involved in salary sacrifice agreements such as fringe benefits tax (sometimes shortened to FBT), which your employer may also deduct from your wages. However, some types of employers – such as charities – are exempt from this tax. It might be worth getting advice from your employer’s payroll officer or your accountant

Leasing companies often promote the savings on fleet discounts and on the GST component of both the vehicle cost and the running costs when you enter a novated lease. You need to pay attention to the total package cost. Other costs, such as interest, administration charges and services fees might outweigh the fleet or GST savings.

Leasing companies often have online calculators that show savings on a novated lease when compared with a traditional car loan. However, these calculators often omit the employer’s fringe benefits tax, which may end up being passed onto you. So you need to factor in this additional cost

Make sure you understand what will happen if you quit, get fired or leave your current employer for the duration of the novated lease. If you change jobs, you may become responsible for the lease payments. Or, you might need to enter into another agreement with the leasing company (this usually means additional administration costs)

Check the residual value or “balloon payment” that applies to your novated lease (remember, this is the amount you can pay at the end of the lease to take ownership of the car). This amount is set by the Australian Taxation Office.

Advantages and disadvantages

There are advantages and disadvantages to novated leases, just as there are to traditional car loans.

So it’s important to fully understand the choice you are making, and the risks involved.

If you’re planning on keeping your vehicle long term, a car loan may be the cheaper option.

If you want to upgrade regularly, a lease may be the convenient way to go.

Either way, make sure you get proper advice and make an informed decision.