What is a Florida reinsurance all about?

What is a Florida reinsurance all about? | Insurance Business America

Guides

What is a Florida reinsurance all about?

With the state’s home insurance rates rising at astronomical levels, is the Florida reinsurance market to blame? Read on and find out

Florida has a unique property insurance market consisting mostly of small and medium-sized local insurers that rely heavily on reinsurance. These companies serve to fill the gap left by national insurers that have shied away from providing coverage in the state because of the enormous risks. For these local insurers, reinsurance functions as a form of a “financial shock absorber,” allowing them to take on more risks often far beyond what they are willing to bear.

In this article, Insurance Business delves deeper into the Florida reinsurance market. We will explain how reinsurance works, what role it plays in the state’s property insurance sector, and how recent events have impacted premium prices. We also encourage insurance professionals to share this guide with their clients to help them understand how reinsurance affects their coverage.

Reinsurance is often described in the industry as “insurance for insurance companies.” For some insurers, reinsurance is an important financial tool that enables them to manage risks and the amount of capital they must have to assume those risks.

The National Association of Insurance Commissioners (NAIC) defines reinsurance as a contract between a reinsurer and an insurer where the insurance company – also referred to as the cedent – transfers risk to the reinsurance company, which assumes a portion or the entirety of one or multiple policies issued by the insurer.

There are several reasons for entering into a reinsurance agreement, according to NAIC. These include:

Expanding the insurer’s capacity

Financing

Spreading risk

Providing catastrophe protection

Withdrawing from a line or class of business

Stabilizing underwriting results

Acquiring expertise

Just like insurance policies, reinsurance can be purchased directly from a reinsurer or arranged through a third-party or an intermediary, aptly called a reinsurance broker. However, insurance companies are not the only ones that purchase reinsurance. Reinsurers also take reinsurance to avoid taking on too much risk in one location. This form of protection is called retrocession.

In Florida, reinsurance takes up almost two-thirds of an average local insurance company’s premiums, according to recent data. But because of the state’s unique profile, reinsurance companies are careful not to assume too much risk, often taking on only a small portion of an insurer’s risk. This practice prompts insurance companies to cede risk to several reinsurers.

The insurance sector comes with its share of jargon, which can be confusing to consumers. If you’re struggling to make sense of industry buzzwords, our glossary of common insurance terms can help.

In general, increases in reinsurance costs incurred by insurance companies are passed on to the policyholders in the form of higher premiums. In Florida, the increasing frequency and severity of natural catastrophe claims have driven up reinsurance rates. Reeling from the insurance aftermath of Hurricane Ian, reinsurance rates have gone up between 45% and 100% in January and another 20% to 40% in the June renewals.

The devastation caused by Hurricane Ian has resulted in almost $114 billion in inflation-adjusted losses, making it the third-costliest tropical cyclone in the US. Losses due to Hurricane Ian trail only those of Hurricane Katrina in 2005 ($192.5 billion) and Hurricane Harvey in 2017 ($152.5 billion), according to data from the National Oceanic and Atmospheric Administration (NOAA).

The state has already placed six insurers in receivership due to insolvencies in 2022 and a few more this year because of losses caused by Hurricane Ian. Dozens of insurers are also on the Florida Office of Insurance Regulation’s (FLOIR) “watch list” due to financial instability. You can check out the complete list of insurance companies in receivership, as well as those that have shut down operations on this website.

Weather-related events have become stronger in recent years, primarily due to climate change, and coastal regions such as Florida bear the brunt of the impact. But between 2006 and 2017, reinsurance costs across the state went down as it experienced only a few destructive storms.

Aiming to ease the financial burden brought about by rising reinsurance costs to both the insurers and their policyholders, Florida has recently passed bills creating reinsurance assistance programs. These include:

Reinsurance to Assist Policyholders (RAP) Fund

The RAP Fund aims to reimburse 90% of an insurance company’s covered losses and 10% of its loss adjustment expenses up to the limits of coverage for two hurricanes that cause the largest losses during a contract year, which runs from 2022-2023 and 2023-2024.

The RAP Fund provides a $2 billion reimbursement layer of reinsurance for hurricane losses, an amount that is significantly lower than the $8.5 billion mandatory layer of the Florida Hurricane Catastrophe Fund (FHCF).

Florida Optional Reinsurance Assistance Program (FORA)

FORA is an optional hurricane reinsurance program that allows insurance companies to purchase reinsurance at between 50% and 65% of the rate online.

Worsening catastrophe claims are driving up Florida reinsurance costs, which has a direct impact on home insurance premiums. It also doesn’t help that the state’s geographic location places it in the path of many devastating storms. Already, Florida homeowners are paying around $6,000 in annual premiums – about four times higher than the national average of $1,700, according to figures from the Insurance Information Institute (Triple-I).

The institute’s recent analysis has revealed that the situation is more of a man-made crisis rather than being caused by Florida’s exposure to extreme weather-related events. Triple-I listed two factors that have pushed the state’s property sector to an insurance crisis:

1. Overly litigious property insurance system

Data gathered by Triple-I has shown that despite accounting for less than a tenth (9%) of all homeowners’ claims in the US, Florida tops the country when it comes to insurance-related litigation, taking up almost four-fifths (79%) of the nation’s total.

The group attributed the situation to a “legal system that invites litigation,” where insurers are required to pay the attorney fees of policyholders who successfully sued over claims – also called “one-way attorney fees” – while also shielding the policyholders from paying the fees when they lose.

A law repealing this practice has since been enacted during the state’s late 2022 special session, resulting in a significant drop in insurance-related lawsuits that home insurance providers have received. The legislation, however, is not retroactive. This means all policies in force before January 1, 2023 will still fall under the previous regulations, including a large volume of disputed claims related to Hurricane Ian.

2. Misuse of assignment of benefits

In an assignment-of-benefits agreement, also called AOB, homeowners agree to sign over their claims to contractors who then work with insurance companies. But what was a standard practice in the industry has become what Triple-I described as a “magnet for fraud.”

With one-way attorney fees eliminating financial accountability from insurance plaintiffs, the system has also encouraged unscrupulous contractors to solicit unwarranted AOBs from unsuspecting homeowners. These contractors then proceed to conduct unnecessary expensive work, file a claim, and sue the insurer when the claim is disputed or denied without the need to inform the policyholders.

The recent legislation also eliminated AOBs, resulting in a significant drop in fraudulent claims.

However, there are several other factors contributing to rising home insurance rates. If you want to learn more about the reasons why Florida insurance rates are going up, you can check out this guide.

Here’s a short report on the Florida reinsurance market and the challenges it faces:

The recent legal reforms designed to reduce claims litigation in Florida have prevented reinsurance companies from pulling out from the property-catastrophe coverage market, abating fears of widespread reinsurance shortage. Although reinsurance rates still rose by double figures, most Florida home insurers were able to secure coverage.

Reinsurers, however, are taking a cautious approach, waiting for proof that the legislative changes work before committing more capacity or considering price decreases. But this wait, according to experts, could lead to frustration among many of the state’s homeowners. They may find it difficult to understand why the new laws did not have a more immediate impact on the premiums they pay.

Industry experts also noted that reinsurance companies will closely monitor the financial stability of ceding companies, especially with several Florida insurers shutting down. Vulnerable insurance providers may have had to pay half or their entire premium upfront instead of the traditional quarterly installments.

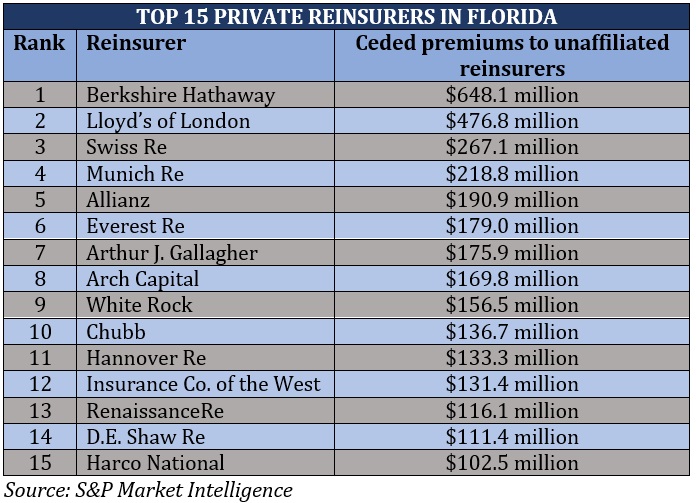

S&P Market Intelligence recently published a list of the top private reinsurers with the largest potential exposure to Florida’s residential property risks. Here are the top 15 reinsurance providers ranked by ceded premiums to unaffiliated reinsurers.

Despite huge catastrophe losses, the global reinsurance market remains robust with major industry players seeing a rise in gross written premiums. Find out which firms made the latest rankings of the 50 largest reinsurance companies in the world by clicking the link.

What are your thoughts about the Florida reinsurance market? Do reinsurers play a crucial role in helping drive down insurance costs? Feel free to key in what you think in the comment box below.

Related Stories

Keep up with the latest news and events

Join our mailing list, it’s free!