What does equipment insurance cover?

What does equipment insurance cover? | Insurance Business America

Guides

What does equipment insurance cover?

Equipment insurance is essential for businesses that depend heavily on their tools and equipment to keep operations running

Equipment insurance is a crucial form of coverage for businesses that rely heavily on their tools and equipment to keep their operations running. It pays out the cost to repair or replace essential items if these are accidentally damaged or lost. But this type of policy offers a broad range of protection. Understanding what’s covered and what isn’t is key to finding the right coverage for your needs.

In this article, Insurance Business digs deeper into what equipment insurance covers. We will give you a walkthrough of what items are included, which incidents are covered, and what costs your policy will pay for. Read on and learn more about how this important form of business insurance can protect you.

Equipment insurance covers a wide array of tools and equipment used in your business’ daily operations. Coverage ranges from small devices to large machinery as long as these items meet three major criteria:

1. The items must be movable.

Equipment insurance is a type of inland marine insurance, which covers goods while they are being transported on land. This means that it covers only items that can be moved from one place to another, usually from your business’ primary office location to different job sites.

Equipment insurance is also referred to as contractor’s tools and equipment insurance or equipment floater insurance. As the second name suggests, it is a floating policy, meaning coverage “floats” with your equipment wherever it goes.

2. The items must be less than five years old.

Equipment insurance policies pay out for the repair and replacement costs of your tools and equipment in two ways:

Actual cash value (ACV) equipment insurance: Pays for the fair market value of the item at the time of the loss, meaning the value of the item when it was purchased minus depreciation.

Replacement cost value (RCV) equipment insurance: Pays out an amount equal to how much it would take to replace the lost or damaged item with a new one.

Most policies provide coverage for tools and equipment that are less than five years old. Some policies, however, also pay out the repair and replacement costs for older items, but only on an actual cash value basis. So, eventually your tools and equipment will age out of the replacement value option.

3. The items must be worth less than $10,000.

Most equipment insurance policies have a coverage limit of $10,000, which is the maximum amount it will pay for the policy period. High-value, top-of-the-line equipment is rarely covered. But for policies that do, coverage usually comes at a steep price.

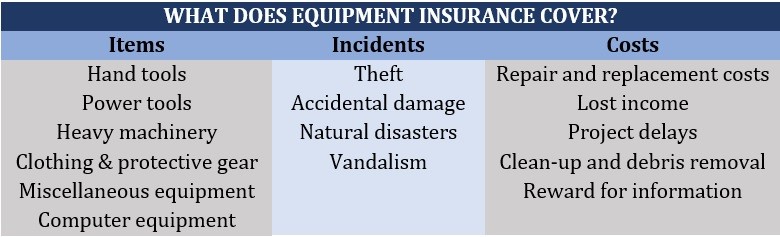

Equipment insurance – covered items

Equipment insurance covers a vast range of items from small manual tools to large machinery. Here’s a list of the different categories that such policies typically cover.

Hand tools: Axes, chisels, digging bars, hammers, hand saws, levels, pliers, screwdrivers, shovels, spades, tape measures, trowels, and wrenches

Power tools: Air compressors, angle grinders, biscuit joiners, circular saws, drills, impact drivers, jackhammers, nail guns, and reciprocating saws

Heavy machinery: Backhoes, bulldozers, cement mixers, compactors, cranes, excavators, forklifts, graders, pavers, tractors, trenchers, and wheel loaders

Clothing and protective gear: Hard hats, hearing protection, high-visibility vests, protective clothing, respirators, safety gloves, safety goggles, safety harnesses, and safety shoes

Miscellaneous equipment: Hand trucks, ladders, sawhorses, scaffolding, stand lights, toolboxes, wheelbarrows, and workbenches

Computer equipment: Camcorders, copiers, desktop computers, laptops, monitors, projectors, and tablets

Some policies also cover tools and equipment that your business borrowed or rented.

Equipment insurance – covered incidents

Equipment insurance is often written on an all-risks basis. This means that coverage may include incidents not specifically listed in your policy document. Some of the events most tools and equipment insurance policies cover include:

Theft: Policies cover incidents of theft that occur on the job site, while your tools and equipment are being transported, and while they are inside a storage facility.

Accidental damage: Instances where an employee unintentionally breaks or damages equipment while doing their jobs are covered. Policies also pay out loss or damage caused by unforeseen incidents such as a water leak damaging your power tools or computer equipment.

Natural disasters: Equipment insurance covers loss or damage caused by natural calamities such as storms, hail, lightning, and wildfire. Depending on the location, some policies don’t automatically include flooding and earthquake damage, although coverage can be extended through riders.

Vandalism: Acts of vandalism that cause damage to your tools and equipment while on transit or at the job site are covered.

Equipment insurance – covered costs

Tools and equipment insurance provides your business with the necessary financial protection in the event equipment damage threatens to derail your operations. Here are some of the costs covered by these policies.

Repair and replacement costs: Depending on how old the items are, equipment insurance may pay out the actual cash value or replacement cost value of your tools and equipment. Items less than five years old are usually paid on a replacement value cost basis, while older equipment is covered on an actual cash value basis.

Lost income: Some policies pay out for the income that you lost because equipment damage has caused your operations to stop. Coverage usually starts from the time of the incident until the equipment has been repaired or replaced.

Project delays: Equipment insurance covers additional expenses your business incurs due to a project delay caused by damaged equipment. Some policies also provide coverage for additional supplies or services needed to keep the project on schedule.

Clean-up and debris removal: If equipment damage causes a major mess, some policies pay out for the cost to clean up or remove the debris.

Reward for information: Some equipment insurance policies will reimburse you for the cost of a reward that leads to the return of stolen equipment or the arrest of the thief.

The table below sums up what an equipment insurance policy covers.

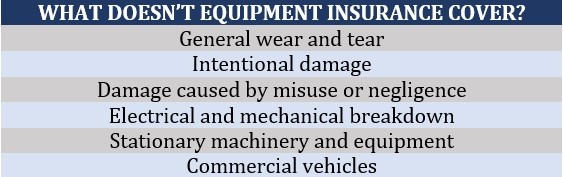

Equipment insurance, however, doesn’t cover every device and machinery that you use for your business and every incident that causes damage. Here are some of the common exclusions from your tools and equipment policy:

Normal wear and tear: Policies don’t pay out if the damage is caused by natural deterioration. These include rust, corrosion, and electrical or mechanical breakdown.

Intentional damage: Equipment insurance will not cover tools and equipment that are deliberately damaged by your staff. Similarly, if the items are misused or damaged because of negligence, your policy will not pay out for the cost to repair or replace them.

Electrical and mechanical breakdown: Equipment insurance doesn’t typically cover electrical or mechanical breakdown, although some policies may allow you to extend coverage at an additional cost. For these types of damage, you need a separate policy called equipment breakdown insurance.

Stationary equipment: Tools and equipment insurance covers only items that can be transported to different worksites. Immobile equipment and machinery are not covered, although these may be included in equipment breakdown policies.

Commercial vehicles: The vehicles your business uses to transport staff and other people are not covered under equipment insurance. These may include cars, trucks, and vans. For these types of vehicles, you need to take out commercial auto insurance.

Here’s a summary of what tools and equipment insurance doesn’t cover.

Equipment insurance is a type of policy designed to cover the repair or replacement cost of the tools and equipment essential to your business if these were stolen, vandalized, or accidentally damaged.

Coverage may seem straightforward but because of similar elements and overlapping inclusions with other policies, it is sometimes confused with other types of insurance. Here are some of the common misconceptions about tools and equipment insurance.

1. Equipment insurance is the same as inland marine insurance.

Tools and equipment insurance is actually a type of inland marine insurance, which covers goods being transported over land. While inland marine policies cease coverage once the items have arrived at their destination, equipment insurance’s coverage extends to when the tools and equipment are used on and stored at the job sites.

2. Equipment insurance covers mechanical and electrical breakdown.

Most policies don’t cover mechanical and electrical breakdown, which are covered under a different type of policy called equipment breakdown insurance. Some equipment insurance policies, however, can be extended to cover for mechanical or electrical failure.

3. Tools and equipment are covered under commercial property insurance.

Standard commercial property insurance covers the tools and equipment that you use for your business as long as they stay inside your primary office location. However, they are no longer covered once they leave the premises. That’s why having equipment insurance is important for businesses that move essential tools and equipment from their headquarters to different worksites.

Equipment insurance is not legally required, although other businesses may make it a condition before agreeing to work with you to protect their investments.

You can purchase tools and equipment insurance as a standalone policy or as a rider to your commercial property insurance or business owner’s policy. The latter is a type of small business insurance consisting of general liability insurance, commercial property insurance, and sometimes business interruption coverage.

Businesses that depend heavily on their tools and equipment to keep their operations running smoothly can benefit from equipment insurance. This type of coverage allows your business to resume work quickly if an essential equipment or tool is stolen or damaged.

Equipment insurance is particularly beneficial for these types of businesses:

Cleaning and janitorial services

Construction businesses

Contractors

Heating, ventilation, and air conditioning (HVAC) technicians

Landscaping businesses

Professional installation services

Tradespeople, including carpenters, electricians, and plumbers

Any business that relies on computers and other electronic devices and equipment

Most equipment insurance policies have a maximum coverage limit of $10,000, but there are some that allow you to raise the limit to cover for more expensive equipment. If you’re currently working out how much coverage your business needs, here are some factors that you need to consider:

If you’re operating a start-up or a small business, then you know shutting down operations can prove costly. But taking out several policies to keep your business properly protected can put a dent on your earnings. That’s why proper planning is important when working out the coverage you need. If you’re concerned about how much you’ll need to pay for coverage, our guide to how much small business insurance costs can help.

The answer to this question depends on whether equipment insurance provides sufficient coverage for the tools and equipment that are essential to keep your business running. Apart from paying for the cost to repair or replace damaged or lost equipment, such policies offer financial protection if equipment damage results in lost income or project delay.

Some policies, however, are restrictive on how much coverage they offer, which explains their relatively low premiums. This may not be a concern if your business doesn’t own specialized, top-of-the line equipment. If your business relies on standard tools and machinery, then equipment insurance may be a worthwhile investment.

But tools and equipment insurance is just one of the several types of coverage that your business needs to be fully protected. If you want to learn more about the other forms of policies business should have, you can check out our comprehensive guide to business insurance.

Do you think equipment insurance is an important form of cover? Tell us why or why not in the comments section below.

Keep up with the latest news and events

Join our mailing list, it’s free!