Wage Protector – Income Protection for High Risk Workers

In our delightful capitalist society, the magic money machine of life is the one thing you depend on most.

And sure, you can’t buy happiness, but money definitely helps.

It’s why your income is so important – and why we spend all that time going to school and potentially onto college so we can get to work.

Work hard.

Make money.

Live well.

But what happens if you can’t work for a long time?

Maybe you’re in a car accident, experience depression or fall ill.

That magic money machine is about to stop chugging out the good stuff.

It’s why Income Protection is so important.

It’s the daddy of all insurance products and will pay you up to 75 per cent of your salary if you can’t work long-term due to any illness, accident or disability.

But if you work a job that insurers categorise as risky (specifically Class 3 and 4—see below), you might face higher premiums.

Which might lead you to believe insuring your income is out of reach.

This is where Wage Protector can help.

What Counts as Class 3 and 4 Occupations in Income Protection?

A quick introduction: all insurers use underwriting to set the cost of your premiums, which is how much you’ll pay monthly to be insured.

Underwriting is a complex mix of math, science, and risk analysis.

The underwriters assess your risk based on your family history, current health, and job. If they believe there is a bigger chance of a claim on your policy than the general population, you’ll pay more.

When comparing Income Protection insurance options here in Ireland, the most important thing here is your job type.

If, for example, you work in bomb disposal, it’s safe to assume the insurers won’t be in a rush to cover you.

On the other hand, you might be surprised to hear that teachers or nurses could face higher premiums than expected.

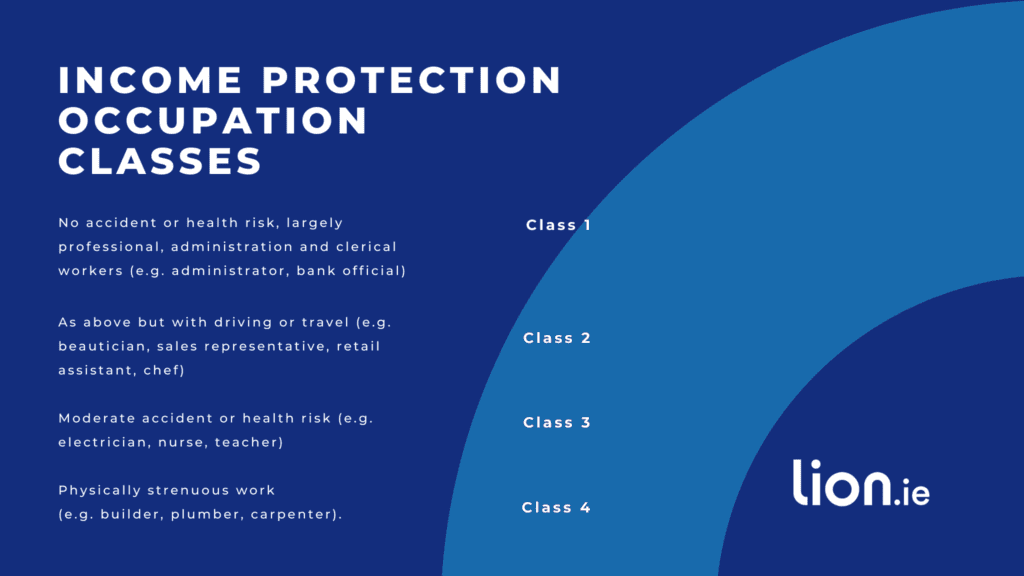

The classes rank from 1 to 4, comme ci:

The insurers rank occupations based on their history of claims and the risk of injury in that occupation.

Class 1 is your standard desk jockey. Accountants, for example.

Class 2 is an occupation that involves some additional risk of injury—a dentist (back/neck issues and stressful occupation) and a sales assistant (lifting boxes) fall into this category.

Class 3, then, involves non-manual and manual occupations. Nurses, teachers, mechanics – you get the gist.

Class 4 is for manual labourers. This includes jobs like general operatives, builders, and tradesmen.

If you fall into Class 3 and Class 4, expect your premiums to be more expensive.

However, Wage Protector is here to make things a bit easier on your póca.

What is Wage Protector?

Wage Protector is a type of income protection which pays you a regular income if you suffer any illness, injury or accident which prevents you from doing your job.

You pay a monthly premium based on your health, your occupation and the level of benefits you want.

It sounds very much like income protection, right?

In fact, when you read that definition, it’d be fair if you thought that they were the same thing.

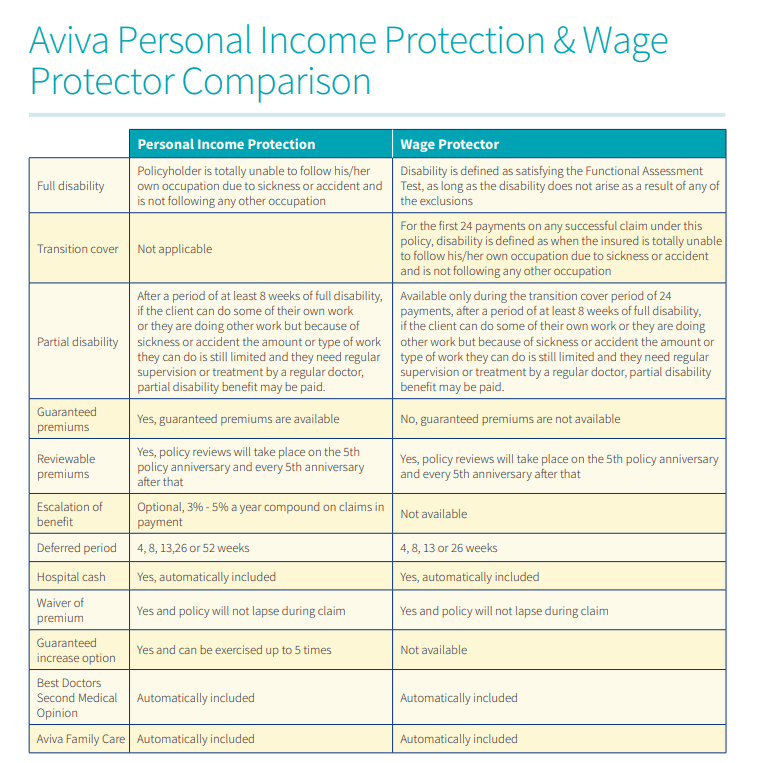

The big differences between Income Protection and Wage Protector are

the price

and how long Aviva will pay you (see below).

Income Protection can seem relatively expensive for Class 3 and 4 workers. As explained above, they are at a higher risk of injury, so the chances of a claim are higher, so the insurer charges more.

From an actuarial viewpoint, this is all fair, but from your wallet’s viewpoint – it’s not so good.

So, to make income protection more accessible to higher-risk workers, Aviva offers Wage Protector.

Your policy will protect you in two ways:

Years 1 to 2 (Transitional Cover)

If you cannot do your job for up to two years, your policy will pay you a replacement income. This gives you an opportunity to get back on your feet or prepare for an alternative job. After this initial period, depending on their circumstances, full Disability Cover may apply.

Here’s a handy chart illustrating the differences between Income Protection and Wage Protector

One thing worth noting is that the deferral period is slightly different. This is the number of weeks you have to be off work before you get paid.

For traditional Income Protection, it’s 4, 8, 13, 26, or 52 weeks.

For Wage Protector, 52 weeks isn’t an option.

You can claim tax relief on both Income Protection and Wage Protector (20 or 40 per cent), which means your premiums may be less than you expect.

Who Qualifies for Wage Protector?

Wage Protector is available if you work in a Class 3 or 4 Occupation.

Because it offers cover for 24 months, it’s less expensive than full income protection, which would pay you until retirement age if you could no longer work.

It offers people who work in riskier jobs, which are generally more expensive to insure, an opportunity to have cover for the first time.

Why Would You Need Wage Protector?

Some employers offer some form of sick pay, but four weeks is considered generous – yep, that’s where we are (check with your own HR department to confirm)

Legally, employers in Ireland don’t have to offer any type of sick pay, while state sick leave covers you for just 5 days.

After that, you may be entitled to a State Disability Benefit of €232 per week, which would significantly lower most people’s incomes and living standards.

With Wage Protector, you will receive a replacement income if you can’t do your job for over 13 weeks.

This means that money is less of a worry, giving you the time to focus on getting better and getting back to work.

How Much Does Wage Protector Cost?

Compared to income protection, it’s a LOT less.

Let’s take two examples: a nurse and a carpenter.

Example 1: Nurse

35 years old

€2000 per month cover

Waiting Period 13 weeks

Covered to age 65

Income Protection: €53 per month (after tax relief)

Wage protector is half the price at €25 per month (after tax relief)

Example 2: Carpenter

40 years old

€3000 per month cover

Waiting Period 13 weeks

Covered to age 65

Income Protection: €76 per month (after tax relief)

Wage protector comes in at €41 per month (after tax relief)

Do you get anything else from Wage Protector?

A puppy!

There is no puppy.

If you want a puppy, you should get one.

But remember that, unlike children, a puppy isn’t just for Christmas.

With Aviva, if you choose Income Protection or Wage Protector, you automatically receive several solidly sound extras.

Forthwith (imagine me saying that as I doff an elaborate top hat):

Best Doctors Second Medical Opinion: You can get a detailed second opinion on any treatment or diagnosis you might have so that you know you’re on the right path with your health.

Aviva Family Care Benefit: A counselling and support service for you and your family if needed.

Hospital Cash Benefit. Literally, an income if you’re in the hospital for more than a week during the deferred period (so some cover before your actual cover kicks in).

Waiver of Premium. You don’t have to pay for cover if you’re out of work (sound)

Proportionate Benefit. If you return to work and your earnings are less than they used to be, you’ll still receive income protection to make up the difference

Relapsed Benefit. If you have to take time off for the same reason within six months of returning to work, the insurer will restart your claim. You don’t have to serve another deferral period.

Over to you…

Fear not, gentle reader.

If you’ve applied for Income Protection before and didn’t go with it because it was too expensive, it’s worth taking Wage Protector a spin.

You can’t use our online quotey-majig to get a quote, but I can get you one—it’s what I was born for—if you fill in this short questionnaire or give me a bell at 05793 20836 on the most useful relic of the past, the good old-fashioned telephone.

Thanks for reading

Nick

Editor’s note: We first published this blog in 2020 and have regularly updated it since.