Using an FHSA to benefit from tax-free growth

Dean is a single Canadian in his twenties looking forward to buying his first home. He’s planning to increase his home savings as his income grows over time. Dean’s advisor recommends a First Home Savings Account (FHSA) because it will give Dean up to 15 years to save, which suits his budget and time frame.

Case Study: Dean

Dean plans to start contributing $150 at the start of each month to his FHSA, eventually getting up to $350 a month in year 14. He keeps his account open for the maximum of 15 years¹ allowed.

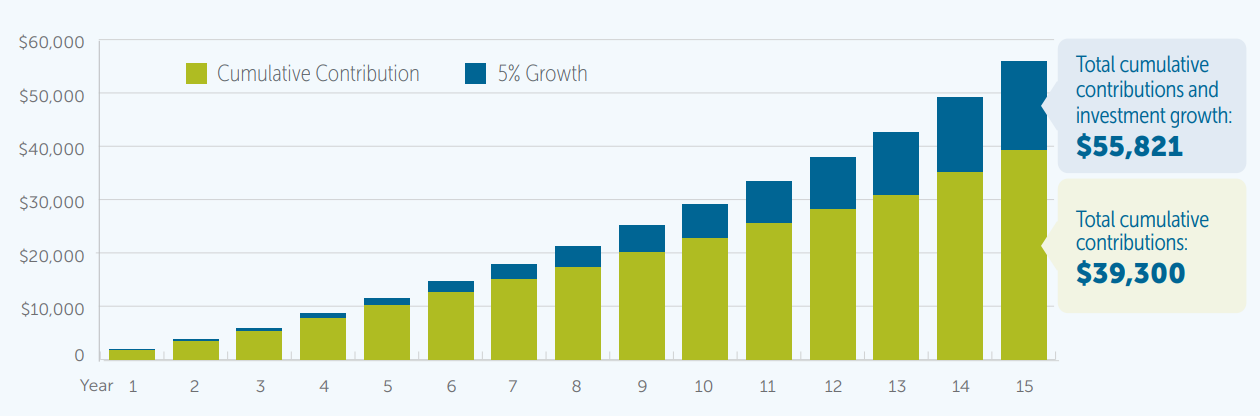

In this example, Dean’s plan goes well, and he’s able to make all the monthly contributions he planned on by setting up a PAD.2 As his income grows, he increases his monthly contributions. At the end of 15 years Dean has contributed $39,300, which is under the lifetime limit of $40,000. Dean is also able to deduct his FHSA contributions from his taxable income each year.

During this time frame if Dean’s investment achieved a rate of return of 5% every year (net of fees), the total market value of his FHSA would be $55,821 after 15 years. If Dean makes a qualifying home purchase, the entire amount can be withdrawn tax-free and used for the purchase of his first home.

Dean’s plan in action

Growth of monthly contributions to Dean’s FHSA for 15 years with 5% growth (compounded monthly)

Chart assumes monthly contributions of $150 in years 1, 2 and 3; $200 in years 4, 5, 6, 7 and 8; $225 in years 9, 10, 11, 12 and 13; $350 in years 14 and 15, with a constant growth rate of 5% per annum compounded monthly.

Why hold an Empire Life segregated fund contract in your FHSA?

Empire Life segregated fund contracts offer flexibility and choice in investment options with up to 100% equity, enabling you to participate in the growth potential of equity markets. Segregated fund contracts offer valuable benefits some other investments cannot, such as maturity and death benefit guarantees, the ability to bypass the estate and probate process if a beneficiary is named, and potential creditor protection.

![]()

To find out if an Empire Life First Home Savings Account is right for you, speak with your advisor or visit empire.ca/FHSA

![]() Download the PDF

Download the PDF

1 Maximum participation period begins when you open your first FHSA and ends on December 31 of the year in which the earliest of the following events occur: the 15th anniversary of opening your first FHSA, you turn 71 years of age, or the year following your first qualifying withdrawal from your FHSA.

2 Pre-Authorized Deposit. Initial Minimum Deposit $1,000 or $50/month per segregated fund.

3 For further information concerning FHSAs, please go to https://www.canada.ca and search for “First Home Savings Account”.

Segregated Fund contracts are issued by The Empire Life Insurance Company (“Empire Life”).

A description of the key features of the individual variable insurance contract is contained in the Information Folder for the product being considered. Any amount that is allocated to a Segregated Fund is invested at the risk of the contract owner and may increase or decrease in value. Please read the information folder, contract and fund facts before investing. Performance histories are not indicative of future performance.

® Registered trademark of The Empire Life Insurance Company.

September 2024