Underinsurance – a big issue for small businesses

Authored by Allianz

Although inflation has moved from its peak at 10.41% in February to 8.68% in May, many businesses are still struggling with inflationary pressures and the cost of living.

Small businesses identified inflation as one of the their biggest concerns for this year and over the past year it’s been found that 51% of businesses have stopped buying at least one insurance cover. In fact, of the 4.3 million SMEs within the UK – it’s estimated around 80% are underinsured.

Underinsurance means the level of insurance you have is not enough – and so it won’t offer the level of financial protection you need.

All businesses are open to risk if they don’t have the correct level of insurance for their needs and may be at risk of financial hardship as a result.

Here are some considerations SMEs can take to help avoid being underinsured.

Property Valuation

Property Owners need to be aware that the current valuation of their property will likely differ from the cost to rebuild it. The amount insured should take into account any rebuild costs, including:

any clearance/removal of debris,the cost of materials and if any specialist materials are required,cost of labour,any professional fees,whether the building is listed

Accurate sums insured

An accurate inventory of a business’ total contents will help establish the right sum insured. This needs to take into account everything in the premises – including customer goods. This should also include seasonal fluctuations, which may be different at peak trading times.

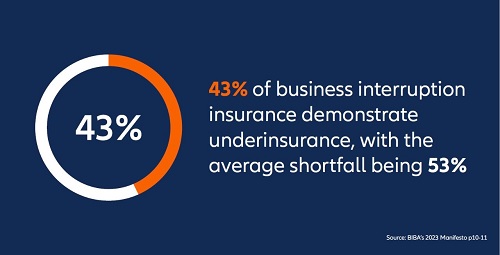

Business interruption

Many businesses underestimate how long it will take to fully recover after a loss, with many opting for a 12-month indemnity period rather than a more generous – and more realistic – 24-month one.

When setting indemnity periods – SMEs should consider:

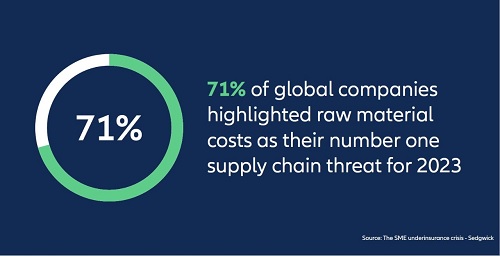

where a business is in a historic or unusual building that may take longer to rebuild or has specialist equipment that can take time to replace.issues around an extended supply chain, which may lead to rebuild times, as well as sourcing replacement items. Especially as supply chain disruptions are set to continue throughout 2023. 4the impact of labour shortagesthat accountancy and insurance policy definitions of annual gross profit are different. Businesses need to make sure their assessment of gross profit matches the one in the policy and that it’s not understated.

Identify gaps in cover

Businesses need to check their cover remains in line with their activities. New risks sometimes emerge so it’s worth considering how the risks to your business change, including areas such as cyber risk or data protection.

Business Continuity

Don’t forget to make sure that disaster recovery or business continuity plans are up to date since they may help you recover more quickly after a loss. Suitable insurance forms a vital part of your business continuity planning.

A regular dialogue between businesses, brokers and insurers is key to helping to ensure SMEs have the appropriate cover. You can read more in our SME Guide to Underinsurance, written in conjunction with BIBA. We also have a wealth of information on our underinsurance and economic insights pages.