Truckers’ Premiums Keep Rising, Despite Safety Improvements, Coverage Changes

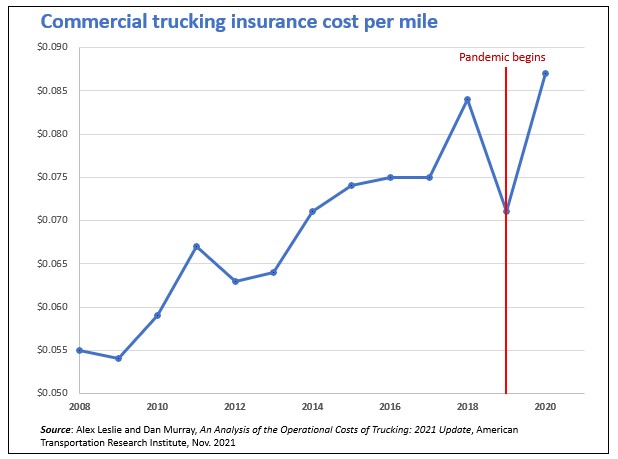

As with so many other goods and services, insurance for commercial trucks has become more costly since the pandemic – but a closer look at the numbers shows that this trend pre-dates COVID-19’s economic and supply-chain disruption.

“Despite reductions in insurance coverage, rising deductibles, and improved safety, almost all motor carriers experienced substantial increases in insurance costs from 2018 to 2020,” according to a recent report by the American Transportation Research Institute (ATRI). And, while frequency and severity have been on the rise from 2009 to 2018, the report shows the rate of insurance cost increases during the period far exceeding the crash rate increase.

ATRI’s observations are consistent with findings in a recent study by Triple-I and the Casualty Actuarial Society (CAS) that the phenomenon known as “social inflation” accounted for $20 billion in commercial auto liability claims between 2010 and 2019.

“External factors that go well beyond carrier safety force commercial trucking insurance costs to increase,” says Triple-I Chief Insurance Officer Dale Porfilio. “The higher premiums ultimately tend to be passed along to consumers in the form of higher prices for goods and services.”

ATRI recognizes three key areas of influence on premiums beyond crash history and policy components:

Economic impacts on the insurance industry,Carrier-specific factors, andSocial inflation.

External economic conditions, including general inflation and rising health-care costs, contribute to increased insurance premium rates.

“Medical advances help save lives, but these treatments directly contribute to higher medical costs,” ATRI points out. “Similarly, technological advances in motor vehicles contribute to increasing costs associated with repairing them; electronics now make up 40 percent of the cost of a new vehicle.”

These higher costs affect premiums through larger claims and losses that have to be incorporated into pricing.

Premium rates also are affected by carrier-specific considerations like operational sectors, cargo values, states or regions of operation, company growth, and commitment to safety culture and technologies.

“Carriers demonstrating consistent year-over-year improvements in safety technology adoption, safe driver hiring and training practices, and crash history can potentially lower their premium costs, despite the current adverse environment,” ATRI said.

“Social inflation” refers to the impact of litigation and government policy trends on insurance claims and, ultimately, costs to policyholders. Social attitudes and behaviors affect insurance payouts through changes in laws and propensity to litigate, and jury awards don’t necessarily reflect logical conclusions or precedents. Jury decisions can be influenced by emotions, state and local laws or procedures, and plaintiff bar tactics. In recent years, practices like third-party litigation funding – investment by hedge funds and other third parties in lawsuits in return for a share in the awards – have played an increasing role in social inflation.