Saving for College: Life Insurance or a 529 Plan?

In the United States, the average cost of a four-year college is $35,720 per student, according to recent data published by the Education Data Initiative. Parents who want to help their children fund at least part of their college tuition often start saving from the minute the child is born. Starting early gives parents time to accumulate a significant sum, which is especially important if you have multiple children.

Many new parents wonder, what’s the best way to save for college? Since there are many savings vehicles available, it can be hard to figure out which will yield the best returns.

In this article, we’ll discuss two popular college savings plans: a 529 plan and life insurance. Each method has its pros and cons, so while we can’t decide for you, we can provide you with the information to help you make an informed decision.

How 529 Plans Work

A 529 plan is designed specifically to help parents save for education, including grades K-12, apprenticeships, undergraduate school, and graduate school. There are two types of 529 plans: education savings and prepaid tuition.

A 529 savings plan (the more popular option) grows tax-deferred. If you withdraw funds from the plan to pay for qualified education purposes, you don’t pay taxes on the withdrawal. The contributions you make are invested in mutual fund or exchange-traded fund portfolios.

A prepaid tuition plan allows you to pay tuition in advance, which has the benefit of locking in the current rate (assuming costs will rise in the future). These plans also have tax advantages, but they are only offered in a handful of states. In most cases, the funds don’t cover room and board, which is something to keep in mind.

What Are the Pros of a 529 Plan?

Like every investment vehicle, a 529 plan has pros and cons. Since only 10 states offer a prepaid tuition 529 plan, we will focus on the pros of education savings plans.

No annual contribution limits – There are no limits to how much you can contribute to your plan each year. While some states limit how much you can contribute in total, the ceiling is quite high, ranging between $235,000 and $529,000.

Tax advantages – Your earnings from your 529 investments are exempt from both federal and state income taxes (as long as you use the money to pay for education). More than 30 states offer tax deductions or credits for 529 contributions as well.

Flexibility – If you have money left in your 529 plan after college tuition has been paid or if your child decides not to go to college, you have several options.

Change the name of the beneficiary (without changing accounts)

Leave the money there in case the current beneficiary decides to use it in the future

Withdraw the funds and use them for something else (and face a 10% penalty—see more about that below.)

Anyone can open a 529 plan – You don’t need to fall into a certain tax bracket to open up a 529 plan. You can open up a plan regardless of your income.

What Are the Cons of a 529 Plan?

While a 529 plan has several benefits, there are also some disadvantages. These include:

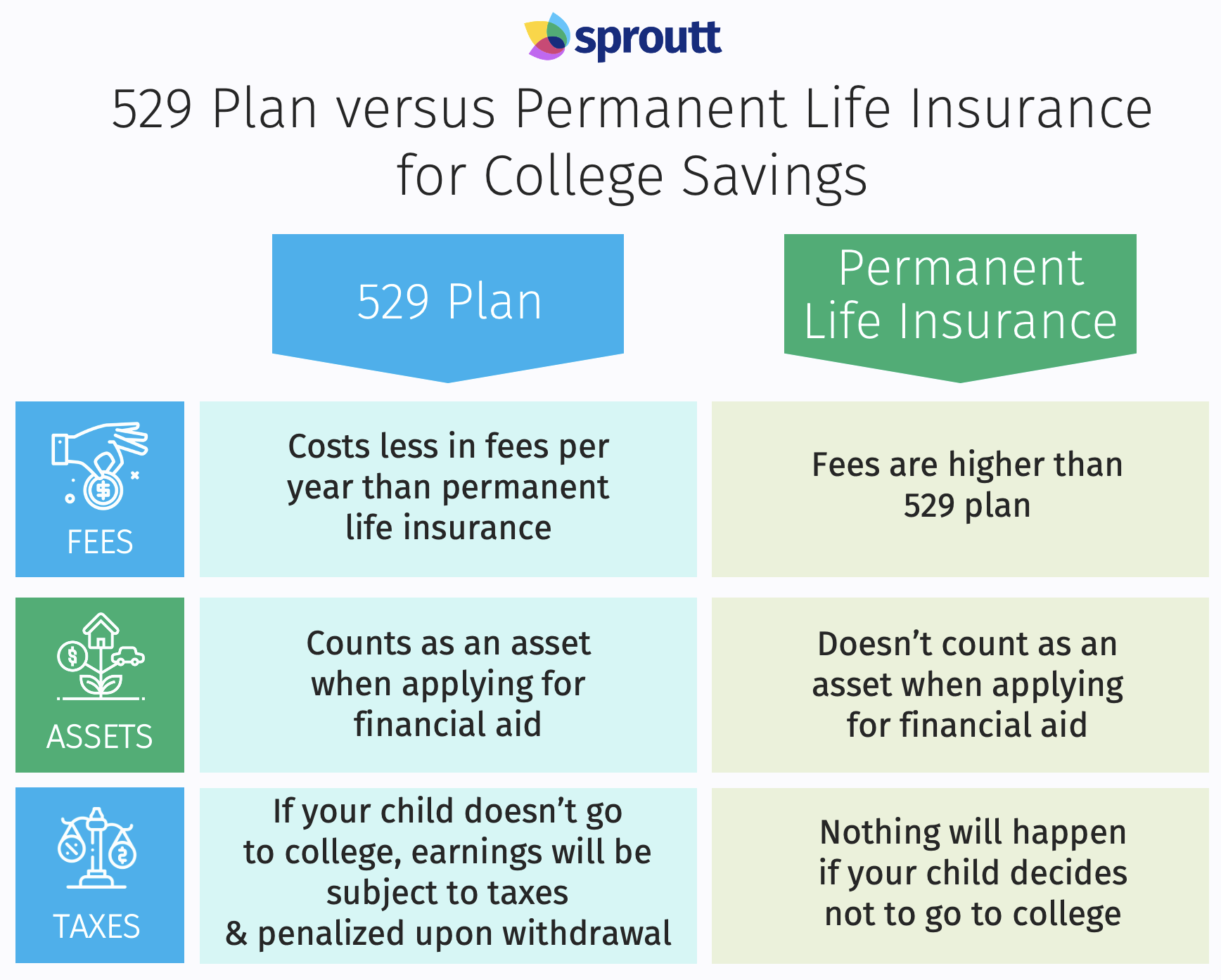

Strict rules about usage – The savings that you accumulate must be used to pay for qualified education expenses. If you use the funds for something else, you’ll be charged a 10% penalty.

Laws vary by state – Each state has its own laws about 529 plans. If you move to a different state, it’s possible that income tax deductions and credits will be subject to recapture in the new state.

Fees – Like most investments, 529 plans have fees. The fees are taken from your contributions, so the higher the fees, the less funds will go to your actual savings account. It’s important to take a little time and search for a 529 plan with low fees.

Financial aid – The savings in a 529 plan count as an asset when your child applies for financial aid for college. The actual impact is greater if your child is the owner of the account, and a little less if you own the account. Either way, 529 ownership has the potential to detract from the financial aid your child qualifies for.

529 Plans: Limited investment options

Since the goal of a 529 plan is to accumulate enough money to pay for college tuition, the investments on the table are relatively low-risk. Some states even offer target-date funds that adjust your investments as your child gets closer to college-age to ensure that there are enough funds.

If you’re someone who has investment experience, you may look at the 529 options and feel limited. In fact, you might even prefer to choose a different type of investment that has the potential to yield more, even if it means forgoing the tax benefits of the 529 plan.

On the other hand, if you’re someone who’s not that financially savvy and prefers to open up a savings account and forget about it, a 529 plan can be the perfect solution. It’s a low-maintenance, straightforward way to accumulate savings. For this reason, having limited investment options is both a pro and a con.

How Permanent Life Insurance Works

Permanent life insurance is another good option for saving for college. Unlike term life insurance, which pays out a death benefit when the beneficiary dies, permanent life insurance offers both a death benefit AND a savings component.

When you pay premiums for permanent life insurance, a portion goes toward the death benefit, another portion goes toward the savings component, and yet another portion is used to pay for administrative fees.

There are several types of permanent life insurance, but whole life insurance is the most popular one.

Pros of Using Life Insurance for College

There are many benefits of using permanent life insurance as an investment, but in this article, we’re zooming in on using the cash value to save for college. Pros of using life insurance to save for college include:

Financial aid – When your child applies for financial aid for college, the savings in your life insurance account are not considered.

Tax advantages – Funds in your permanent life insurance account grow tax-deferred, like those in a 529 plan.

Savings can be used for anything – Unlike a 529 plan, the savings in your life insurance account can be used for anything (beyond college costs). If your child decides not to go to college, you can still use the accumulated cash during your lifetime without being penalized. For example, many people use permanent life insurance to supplement their retirement savings.

Flexibility – There are several ways you can use your savings to pay for your child’s college tuition:

Borrow against the cash value (which is easier than taking out a traditional loan, plus the interest rates are usually lower)

Withdraw a portion of the cash value

Surrender the policy and receive the entire cash value (though you will be charged a surrender fee in this case)

Cons of Using Life Insurance for College

While using permanent life insurance as a way to save for college has several advantages, there are also several drawbacks. The main ones include:

It can be expensive – Permanent life insurance is expensive, significantly more so than term. If you’re looking for affordable life insurance, term is your best option. If you’re looking for a savings account, permanent life insurance is a relatively expensive one to maintain. Its fees can often be more expensive than those of a 529 plan.

Takes time to accumulate cash value – While it’s always best to start a college savings fund as early as possible, with permanent life insurance, it’s essential. It usually takes 10 years for the amount in your cash value savings to surpass the amount paid in premiums, which means you’ll need to buy this type of life insurance before your child is born or immediately after in order for it to be worthwhile as a savings vehicle.

Is Life Insurance a Good Way to Save for College?

Life insurance can be a good way to save for college—for certain people, in certain situations. While there are several benefits of using the cash value of a permanent life insurance policy to fund college tuition, there are also other investment tools, like a 529 plan, that offer their own set of benefits.

The best way to decide if life insurance is the right savings tool for you is to consult with a financial advisor, someone you can trust to guide you in the creation of a solid financial plan. If you’re interested in buying permanent life insurance as a way to save for college AND a way to ensure that your loved ones are covered in case you die, the insurance advisors at Sproutt can give you advice about which type of permanent policy is best.

How Does Permanent Life Insurance Work?

Permanent life insurance is an umbrella category that includes different types of policies, including whole and universal. Whole life insurance is often chosen to pay for college. Most permanent policies accumulate a cash value and last the policyholder’s entire lifetime.

Term life insurance, on the other hand, is a completely different type of policy. It only lasts for a certain number of years, called a term, and doesn’t come with a cash value. Due to the lack of cash value, it shouldn’t be considered if saving for college is your main goal. (However, it’s a good type of life insurance for college students themselves — discussed at length further on.)

The way permanent life insurance works is that a portion of your monthly premium goes toward paying for death benefit coverage and another portion gets deposited into a separate cash value account. The money in the account grows tax-deferred and isn’t considered an asset when applying for financial aid for college.

Accessing the Cash Value of a Permanent Policy

There are several ways to access the cash value of your policy to pay for your child’s college education. You can:

Take a loan against the value of your policy, which you must pay back in full. (If you die before the loan is paid back, the outstanding debt will be taken off the policy’s death benefit.)

Withdraw the cash value, so you don’t need to pay back the loan but you know from the get-go that the death benefit will be reduced.

Surrender the policy and receive the entire cash value. A universal life policy will also have a surrender fee charged by insurers. This is the least ideal option, since your entire policy will be liquidated.

Bottom Line

Yes, it’s possible to use life insurance to pay for your child’s college education. In addition to the death benefit that’s standard to all life insurance policies, the cash value of a permanent policy can be used as a sort of child life insurance college fund. However, there are pros and cons when comparing permanent life insurance to other investment vehicles, namely the 529 plan.

When deciding which investment vehicle to choose, the main thing to keep in mind is that in order for a permanent policy to be a worthwhile savings plan for college, you need to buy it when your child is a baby or toddler.

FAQs

Still have questions? We have answers! Read on to find out more about using life insurance to pay for college.

Can I use life insurance to pay for college?

When the question is being asked by a parent on behalf of their children (i.e., the parent wants to save money to pay for their child’s college tuition), the answer is yes. The cash value of a permanent policy can indeed be used to pay for a child’s college tuition.

However, when the question is being asked by the potential students themselves, the answer is no. In other words, a potential college student may have heard that you can use life insurance to pay for college, and is now considering a policy for that purpose. This won’t work. The policy usually needs to be in place for at least 15 years in order for the cash value accumulation to be worthwhile.

If a student wants to get life insurance while in college, they certainly can. In fact, the younger you purchase life insurance, the lower your rates will be. But the life insurance policy won’t be able to pay for college at that point in time.

What type of life insurance is best for students?

Term life insurance is usually the best life insurance for college students, since permanent policies are significantly more expensive. A term policy is an ideal choice for a college student who has student loans. A life insurance policy can ensure that their debt doesn’t get passed to their parents or loved ones if something happens to them. In this case, the length of the term needs to be based on the number of years it will take to pay back the student loans.

If at some point during the term, the student gets married and/or has kids, they may want to convert their policy to a permanent one or buy an additional term policy to cover their new expense.

For parents buying life insurance as a way to save for their children’s college tuition, whole life insurance is a popular choice for college savings, although some prefer universal. Either way, it’s important for parents to choose a type of permanent life insurance that includes a cash value in order for the policy to be used for college savings.

Does a college student need life insurance?

No one needs life insurance, though it is highly recommended for people who fit certain criteria. Those with significant debt, who are married, have children, or have an independent business venture are strongly recommended to get life insurance. In the case of securing an SBA loan, most lenders will require life insurance, as explained by smartbiz. But this isn’t the case with student loans.

So while it’s a good idea for a college student to get life insurance, for the reasons explained above and in this Forbes article, it’s not mandatory.

How do college students get insurance?

College students get insurance the same way everyone else does. If their parents already have insurance, they can choose to go through the same insurer. If they want to try and get a deal, they can visit Sproutt and get a roundup of the best quotes available.

Does life insurance have to pay off student loans?

Whether you buy a life insurance policy as a parent or a college student with the purpose of paying off student loans, no one will force you to use life insurance for that purpose.

For example, if a parent bought a whole life insurance policy when his child was born for the purpose of paying for college, but then their child got a full scholarship, it’s no problem to use the cash value in that policy for something else. (Bear in mind that if you have a 529 plan and the child doesn’t end up going to college, parents can be penalized with fees.)

If a student took out term life insurance to cover their student loans and then managed to pay them back quicker than expected, the death benefit can be used for other purposes by the beneficiaries.

Can international students get life insurance?

Yes, international students can get life insurance, but their choices are usually limited. Additionally, they must be able to provide legitimate documents to prove their status in the United States, i.e. a green card or a visa. While choices might be limited, international students should consider life insurance for the same reason local students should: to protect their families from student debt.

You can contact Sproutt insurance advisors to find out what your life insurance options are as an international student.