Invasion’s Impact on CPI, P/C Replacement Costs

Russia’s invasion of Ukraine since Feb. 24, combined with persisting supply chain disruptions related to the pandemic, continue to drive inflation as measured by the Consumer Price Index (CPI). From a property/casualty insurance perspective, these forces have a particularly strong impact on replacement costs – especially in the automotive sector.

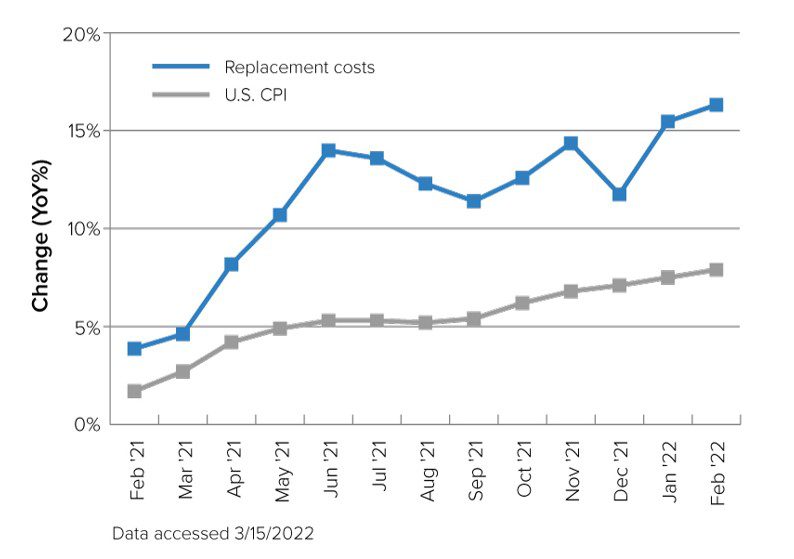

Total P/C replacement costs represent a weighted average for the homeowners, personal and commercial auto, commercial multi-peril, general liability, and workers compensation lines. Auto replacement costs include new and used vehicles, as well as parts and labor for construction and repair.

Based on the March release of CPI data from the Bureau of Labor Statistics, total P/C replacement costs rose to 16.3 percent in February – up 4.6 percent from 11.8 percent in December. That increase is 3.3 percent greater than Triple-I projected in December, before the invasion began.

While CPI growth is largely being fueled by rising gasoline prices stemming from uncertainty surrounding affairs in Eastern Europe, the key driver of replacement costs is the industry’s exposure to auto prices. New-vehicle price increases only broke double-digits in the fourth quarter of last year; however, used-vehicle price inflation has been above 25 percent in nine of the past 12 months.

“Despite fuel imports from Ukraine and Russia making up only a single-digit percentage of U.S. energy consumption, gasoline prices will likely remain elevated as speculation over OPEC exports, alternative fuel sources for Central Europe, long-term profitability of domestic drilling operations, and rising food-insecurity in fuel exporting counties in the Middle East continue,” said Dr. Michel Léonard, Triple-I’s chief economist and data scientist and head of its Economics and Analytics Department. “At the same time, new vehicle prices can be expected to keep rising as Russian exports of nickel and palladium cease.”

Russian exports of these metals – critical to automotive construction – account for 15 percent and 20 percent, respectively, of the global market.

Dramatic increases in used vehicle prices are common during and after economic corrections and recessions, Léonard said, adding that these elevated prices usually resolve themselves within 24 months of the end of the downturn. Assuming the supply-chain situation improves and the U.S. economy doesn’t slip back into recession, used vehicle price growth is likely to fall back in line with new vehicle inflation over the next 12 months.