Income Protection from Zurich Life | Review

Hello, and welcome back to my Insurance Providers Break Down series.

I hope you’re not having a breakdown reading them.

If you missed the previous nail-biting instalment featuring Insurance Bros, Irish Life and their mortgage protection – have at that link, and you can get the rundown on whether it’s a crock of gold or a crock of shiiii.

te.

But today, it’s all about Zurich Life and their income protection what have yous.

So, you’re looking for the best income protection policy the world can offer, you’ve done all the research, you know income protection is the BEE’S KNEES, but you’re still not sold on which insurer to choose, and if you should go with the lads from Switzerland 🇨🇭

I know; it’s like sending your toddler into the sweet shop. They know they want sweets, but which one will best serve their toddler-sized sweet tooth is an almost impossible decision. It’s the same for us and insurance, sort of.

A child would never choose Swiss Chocolate, far too rich and not enough sugar but should you go to Zurich for your income protection?

Let’s see,

I’ve rounded up the top 3 policy benefits on income protection from Zurich Life that might tip the scales in their favour.

First up…. Their Rehabilitation Nurse Team!

Does Zurich Life have Rehabilitation and Retraining Benefits on their Income Protection?

You’d think that all you need when looking for income protection policies is a reliable provider who won’t hold out on the cash when you’re unable to work.

But little extras like these really sweeten the deal.

Zurich Life isn’t just prepared to hand out the wonga when you can’t work, and they want to help you medically too.

They will offer you access to a crack team of rehabilitation nurses who provide medical advice and any support you may need.

Zurich Life is the generous cash granny you’ve always wanted.

But what’s in it for them?

Awkward hugs and constant pecks on the cheek?

Nope, but they want to get you back to work as soon as possible because the longer you’re off work, the longer they’ll have to pay you.

Even before they pay your claim, Zurich Life, and your dedicated claims specialist, will work out if there is anything they can do to help your recovery. You’d be amazed how quickly early intervention can prevent a short term issue from becoming a long term problem.

So what kind of things will they offer you to get you back on that workhorse?

Pain management methods

Arrangements for treatments

Payment for some types of treatments

Create a back to work plan

Yup, they provide some awesome support benefits. However, these benefits aren’t just for you; they’re for Zurich Life too.

Now there are a few other illness-related benefits that I want to skim over before I move to benefit number two.

You don’t pay a premium while receiving a claim.

Like most income protection providers, Zurich Life puts a stop on your premium payments until you can go back to work, so if you’re out in claim, you don’t pay a cent for your cover.

Hospital stay payment.

So say you’ve ended up on an unexpected hospital holiday, Zurich Life, upon day 8 of your stay, will begin to pay you a daily income regardless of whether you have served the deferred period on your policy.

Even if your policy has a deferred period of fifty-two weeks, Zurich will pay you daily if you are in hospital for over eight days.

Are you ready for a bonus….they don’t just pay you from day 8; they will backdate your payments, so you are paid for your entire hospital stay.

So let’s say you bought a policy from Zurich. The very next day a hot air balloon lands on you squashing you like a penny and sending you to the hospital ward for six months.

After 8 days Zurich will start paying your income protection claim, and will continue to pay it for those six months.

Okay, the next benefit up under the interrogation light is….The Salary Top-Up!

What if you get back to work on a lower salary?

This benefit is short and sweet.

You’ve entered the workplace again, but say you’re not fully back to your old self, and so your boss decides only to bring you back part-time until you’re back in tip-top shape.

Well, as thoughtful as that may be, your bank balance won’t be too happy with the prospect of a lower income than you were receiving when you were out on a claim.

In this case, Zurich Life can temporarily top up your salary by continuing to pay your income protection claim on a proportionate basis.

Makes sense? Sweet. On to the last, but by no means least, income protection policy benefit from Zurich Life.

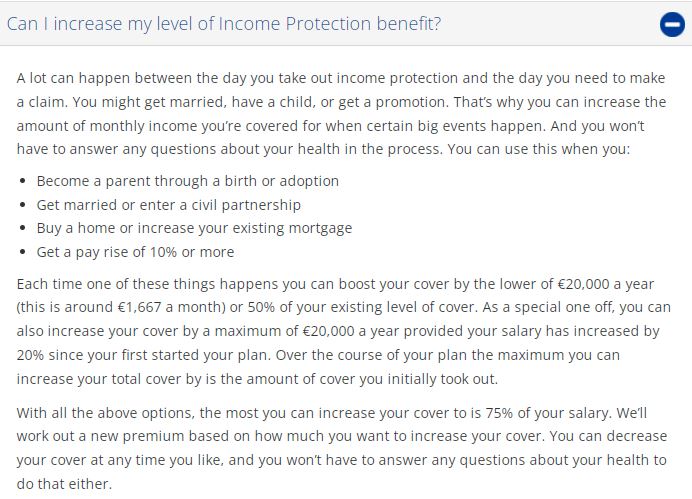

How do you increase your income protection with Zurich Life?

Guess who’s back, back again?

It’s our favourite imaginary couple, Bill and Hilary.

Please give them a round of applause, folks, because they’re about to show you what these nifty protection level increases are.

We meet Bill and Hilary as a very young couple, no kids, haven’t gotten married yet, and haven’t moved in together, but things are going pretty good, so it won’t be long before wobbling angry infants wreck their house, and B&H can’t stand the sight of each other.

But before all that!

They’re going to need income protection to keep up with these changes, right?

Zurich Life can increase their income protection with each of these big life moments.

Becoming a parent (birth or adoption)

Marriage/civil partnership

Pay raise of more than 10%

The income your income protection policy is protecting will change over a couple of decades, hopefully going up, not down.

When Bill and Hilary first met, he was a burger flipper at Maccie D’s, and she was a trainee hairdresser. Not a bob to spare between them, but their parents were gas and bought them some income protection for Christmas.

True story.

But now, 15 years later, Bill’s a high flying legal eagle, and Hilary is Ireland’s most successful hair transplanter.

Definitely a few more bobs to go around now.

Add to that their beautiful bundle of joy, Dermot, and it’s clear their income protection from 15 years ago wouldn’t support their lifestyle now should one of them be unable to work.

Thankfully, Zurich Life has provided them with the opportunity to increase their policies as they pass those life milestones.

As always, there are T&Cs to how these increases work, but c’mere I’m trying to make this stuff semi-interesting, so I won’t bore you with the finer details.

Oh, you want the finer details, do you, fine, pick the bones out of this:

Inflation protection

Finally, there’s another benefit Zurich Life offers that can help with current goings-on.

Take that naughty Inflation that is smacking us all in the chops right now.

You can smack his back by adding inflation protection to your policy.

Your cover will increase with this extra layer of safety by 3% every year. Just bear in mind that your premium costs will increase by 3.5% every year. Ouch!

How does Zurich Life Compare to Other Income Protection Providers?

There are now five income protection providers in Ireland

Aviva – The OG, longest established, assess applications and pay claims fairly, best rehabilitation and retraining benefits in the market.

Irish Life – This allows you to protect payments into an Irish Life pension.

New Ireland – Have an exclusive Confirmed Income Option – if your income falls during the term of our policy, they will pay based on your original income amount.

Royal London – Back to work benefit (if you’re on a claim for over a year, they will pay you 75%, 40% and 25% of your claim in the first three months back to work

Over to you

I bet you didn’t think about all those benefits when considering purchasing an income protection policy.

So, whaddya think?

You sold on Zurich yet?

Still a little confused or overwhelmed?

Don’t stress. I’m here to chat about it all if you need to; schedule a callback here or complete this questionnaire, and I can help you make that income protection decision you’ve been putting on the long finger for far too long.

Thanks for reading

Nick