Illinois Bill Highlights Need for Educationon Risk-Based Pricingof Insurance Coverage

Legislation being considered in Illinois underscores the need for legislators and other policymakers to become better educated about the importance of risk-based pricing and how it works.

The Motor Vehicle Insurance Fairness Act would bar insurers from considering nondriving factors, such as credit scores, when setting premium rates. The prohibitions include factors that actuaries have demonstrated correlate strongly with the likelihood of a driver eventually submitting a claim, as well as ones insurers already are prohibited from using.

This suggests a lack of understanding about risk-based pricing that is not isolated to Illinois legislators – indeed, similar proposals are submitted from time to time at state and federal levels.

Confusion is understandable

Risk-based pricing means offering different prices for the same coverage, based on risk factors specific to the insured person or property. If policies were not priced this way, lower-risk drivers would subsidize riskier ones. Charging higher premiums to higher-risk policyholders helps insurers underwrite a wider range of coverages, improving both availability and affordability of insurance.

The concept becomes complicated when actuarially sound rating factors intersect with other attributes in ways that can be perceived as unfairly discriminatory. For example, concerns are raised about the use of credit-based insurance scores, geography, home ownership, and motor vehicle records in setting home and car insurance premium rates. Critics say this can lead to “proxy discrimination,” with people of color in urban neighborhoods being charged more than their suburban neighbors for the same coverage.

Confusion is understandable, given the complex models used to assess and price risk. To navigate this complexity, insurers hire actuaries and data scientists to quantify and differentiate among a range of risk variables while avoiding unfair discrimination.

Appropriate protections are in place

It’s important to remember that insurers don’t make money by not insuring people. They are in the business of pricing, underwriting, and assuming risk.

Because of the critical role insurers play in facilitating commerce and protecting the lives and property of individuals, insurance is one of the most heavily regulated industries on the planet. To ensure that sufficient funds are available to pay claims, regulators require insurers to maintain a cushion called policyholder surplus.

Credit rating agencies, such as Standard & Poor’s and A.M. Best, expect insurers to have surpluses exceeding what regulators require to keep their financial strength ratings. A strong financial strength rating enables insurers to borrow money at favorable rates – further promoting insurance availability and affordability.

On top of these constraints, state regulators have the authority to limit the rates insurers can charge within their jurisdictions.

No profit, no insurers — no insurers, no coverage

Like any other business, insurers must make a reasonable profit to remain solvent. Because they can’t just move money around as more lightly regulated industries can, the only way to generate underwriting profits is through rigorous pricing and expense and loss controls. Insurers don’t want to overcharge and send consumers shopping for a better price, or undercharge and experience losses that erode their ability to pay claims.

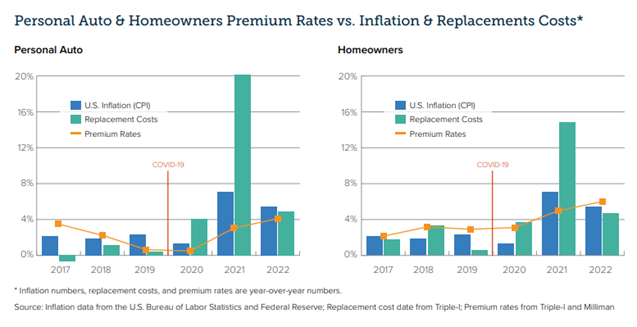

In this context, it’s important to note that personal auto and homeowners insurance premium rates have remained relatively flat as inflation and replacement costs have soared through the pandemic and supply-chain issues related to Russia’s invasion of Ukraine (see chart below).

During this period, writers of these coverages have struggled to turn an underwriting profit. Personal auto has been a primary driver of the overall industry’s weak underwriting results. Dale Porfilio, Triple-I’s chief insurance officer, recently said the 2022 net combined ratio for personal auto insurance is forecast at 111.8, 10.4 points worse than 2021 and 19.3 points worse than 2020. Combined ratio represents the difference between claims and expenses paid and premiums collected by insurers. A combined ratio below 100 represents an underwriting profit, and one above 100 represents a loss.

Even as inflation moderates, loss trends in both of these lines – associated with increased accident frequency and severity in auto and extreme-weather trends in homeowners and auto – will require premium rates to rise. The question is: Will the cost fall evenly across all policyholders, or will rates more accurately reflect policyholders’ risk characteristics?

Protected classes

The United States recognizes “protected classes” – groups who share common characteristics and for whom federal or state laws prohibit discrimination based on those traits. Race, religion, and national origin are most commonly meant when describing protected classes in the context of insurance rating, and insurers generally do not collect information on these “big three” classes. Any discrimination based on these attributes would have to arise from using data that might serve as proxies for protected classes.

Algorithms and machine learning hold great promise for ensuring equitable pricing, but research shows these tools can amplify implicit biases.

The insurance industry has been responsive to such concerns. For example, recent Colorado legislation requires insurers to show that their use of external data and complex algorithms does not discriminate against protected classes, and the American Academy of Actuaries has offered extensive guidance to the state’s insurance commissioner on implementation. The Casualty Actuarial Society also recently published a series of papers (see links at end of post) on the topic.

Correlation matters

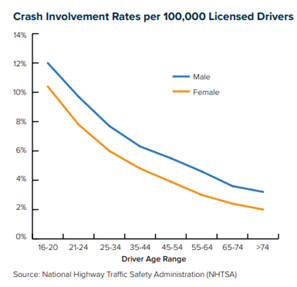

Certain demographic factors have been shown to correlate with increased risk of submitting a claim. Gender and age correlate strongly with crash involvement, as the National Highway Traffic Safety Administration (NHTSA) data illustrated at right shows.

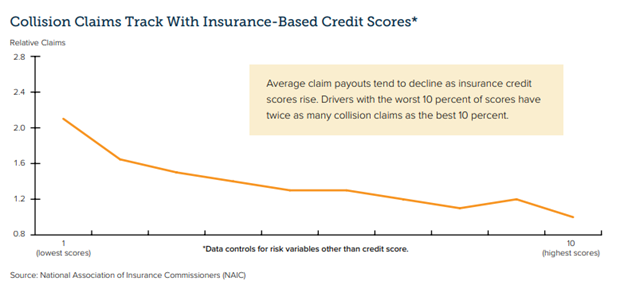

Likewise, National Association of Insurance Commissioners (NAIC) data below clearly shows higher credit scores correlate strongly with lower crash claims.

Similar correlations can be shown for other rating factors. It’s important to remember that no single factor is determinative – many are used to assess a policyholder’s risk level.

Consumers “get it” – when it’s explained to them

A recent study by the Insurance Research Council (IRC) found consumer skepticism about the connection between credit history and future insurance claims appears to decline when the predictive power of credit-based insurance scores is explained to them. Through an online survey with more than 7,000 respondents, IRC found that:

Nearly all believe it is important to maintain good credit history, and most believe it would be “very” or “somewhat” easy to improve their credit score;Consumers see the link between credit history and future bill paying but are less confident about the link between credit history and future insurance claims.After reading that many studies have demonstrated its predictive power, most agree with using credit-based insurance scores to rate insurance, especially for drivers with good credit who could benefit.

If consumers “get it” when you share the data with them, perhaps policymakers and legislators can, too.

Learn More:

Triple-I Issues Briefs

Risk-Based Pricing of Insurance

Race and Insurance Pricing

Personal Auto Insurance Rates

Drivers of Homeowners Insurance Rate Increases

How Inflation Affects P/C Insurance Premium Rates – And How It Doesn’t

The Triple-I Blog

Inflation Trends Shine Some Light For P&C, But Underwriting Profits Still Elude Most Lines

Education Can Overcome Doubts on Credit-Based Insurance Scores, IRC Survey Suggests

Matching Price to Peril Helps Keep Insurance Available & Affordable

Bringing Clarity to Concerns About Race in Insurance Pricing

Delaware Legislature Adjourns Without Action on Banning Gender as Auto Insurance Factor

Triple-I: Rating-Factor Variety Drives Accuracy of Auto Insurance Ratings

Auto Insurance Rating Factors Explained

The Casualty Actuarial Society

• Defining Discrimination in Insurance

• Methods for Quantifying Discriminatory Effects on Protected Classes in Insurance

• Understanding Potential Influences of Racial Bias on P&C Insurance: Four Rating Factors Explored

• Approaches to Address Racial Bias in Financial Services: Lessons for the Insurance Industry