Homeowners Premiums Rise Faster Than Inflation; Expect This to Continue

Homeowners insurance premium rates are rising faster than inflation, S&P Global Market Intelligence data shows, and Triple-I’s chief insurance officer says they’re likely to keep climbing.

From 2017 through 2020, premium rates are up 11.4 percent on average countrywide, according to S&P. Recent factors include rising material costs and supply-chain disruptions that are driving up home-replacement costs — and insurers are adjusting premiums accordingly. The countrywide average annual premium has increased to $1,398 in 2021.

“From everything I know about homeowners’ risk, I expected those numbers to be higher,” Triple-I’s Dale Porfilio told the Washington Post. “Honestly, I would say they still should go up further.”

Most mortgage lenders require borrowers to carry homeowners insurance. According to a recent Bankrate.com analysis, the average homeowner spends about 1.91 percent of household income on home insurance. Location often drives costs up, particularly if the house is in an area prone to natural disasters. Some areas have higher rates because it costs more to rebuild a house there.

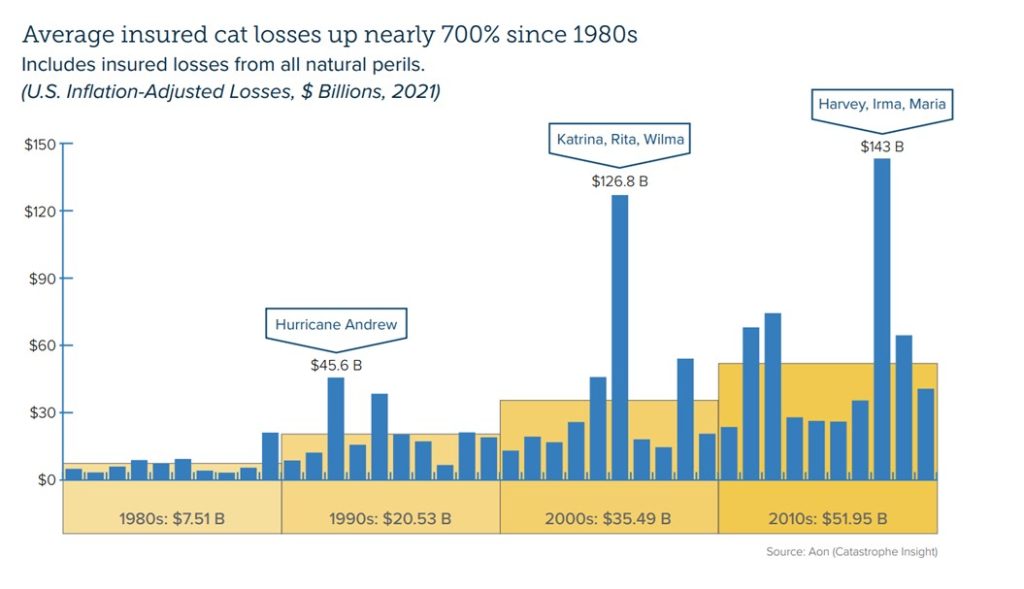

Porfilio said insured damage from tornados, hurricanes, severe storms, wildfires and other natural disasters has reached $82 billion in 2021, bringing the total from 2017 through 2021 to more than $400 billion. As the chart below shows, average insured natural catastrophe losses have increased nearly 700 percent since the 1980s.

“Climate risk is continuing to put pressure on all things weather-related,” Porfilio said. “We are seeing more severe hurricanes, more severe wildfires, and the science isn’t as clear on tornado events in terms of whether they’re changing in frequency or not. But what we definitely do know is that severity is going up.”

When a natural disaster affects a wide area, the demand for materials and labor puts pressure on prices.

On top of the extreme-weather and population shifts that have been driving up insurers’ costs and, in turn, policyholders’ premiums, add the impacts of the pandemic-driven supply-chain disruptions.

“When the pandemic hit, lumber producers feared a repeat of the Great Recession,” the Washington Post reported. “They cut production and unloaded inventory. But demand soared, catching them by surprise. The price of lumber spiked to $1,500 per thousand feet of board in March, a 400 percent year-over-year increase.”

Homeowners can find recommendations for lowering their homeowners insurance costs on Triple-I’s website.