Getting Life Insurance in Ireland with Cardiomyopathy

Complete this questionnaire and I’ll check if cover is possible and send you an indicative quote.

Can You Get Mortgage Protection if You Have Cardiomyopathy?

30 Second Summary

If you are over 35 and have been diagnosed with cardiomyopathy over 3 years ago, we should be able to get you cover.

Outside of this, the insurers will consider on a case by case basis.

If you have a pacemaker or ICD, cover is unlikely, I’m sorry.

What is a Cardiomyopathy?

Cardiomyopathies are a group of heart muscle disorders in which the heart can no longer receive or pump blood effectively throughout the body.

They can be caused by other diseases or idiopathic (unknown cause).

The risks associated with cardiomyopathy can include fainting, breathlessness, fatigue, angina, and, most importantly, sudden death from an insurer’s point of view.

In this article, I’m going to try to answer some of the questions that are running through your head like:

Can you get life insurance if you have cardiomyopathy?

What do you need to do to apply?

What information will the insurer need?

Which insurer is best?

Will I be covered for everything?

How long will it take?

How much will it cost?

1. Can You Get Life Insurance with Cardiomyopathy?

You’ll be relieved to hear that the answer is yes, you can get life insurance with cardiomyopathy, but it’s not straightforward.

And you will have to pay more for your cover than someone in perfect health.

How much more you will have to pay is called the life insurance loading, and I won’t know how much this is until the insurer reviews your medical report.

If you’re under forty, it’s more difficult to get cover.

The insurers won’t cover someone under age 30 with Hypertrophic Obstructive Cardiomyopathy (HCM)

However, cover may be possible for someone over age 30, with idiopathic/familial HCM.

This is assuming they have no complications, and their Left Ventricular function EF is over 50%.

Unfortunately, none of the insurers can offer cover if you have had an Implantable Cardioverter Defibrillator (ICD) or pacemaker fitted, regardless of your age.

2. What If The Cardiomyopathy Was Recently Diagnosed?

If you are over 40, the insurer will wait three years after you have been diagnosed before they will consider cover.

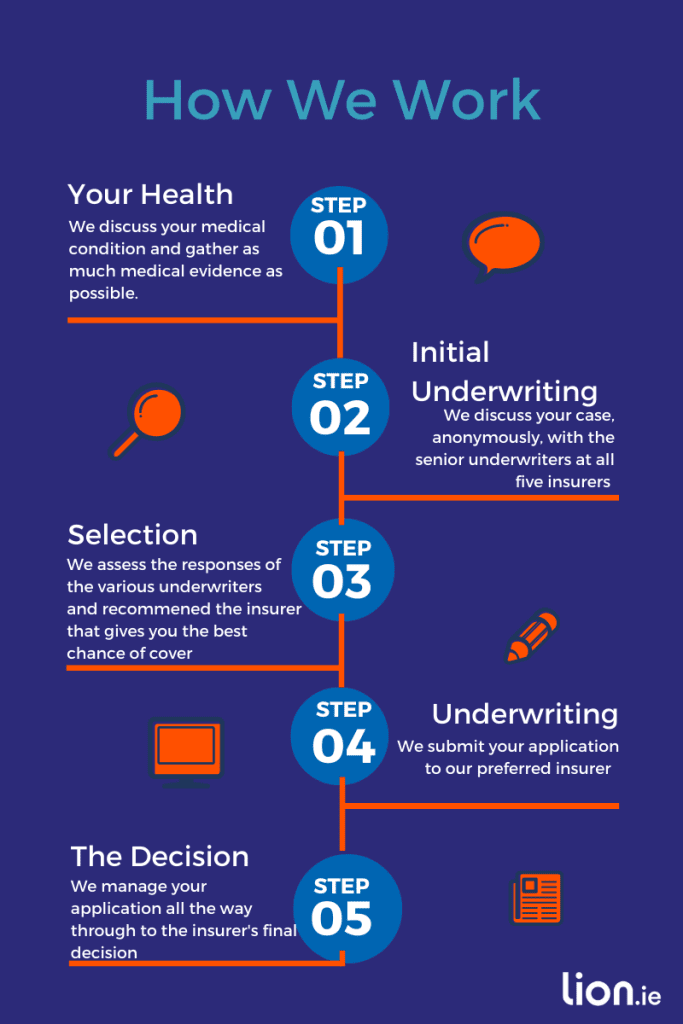

3. What’s The Best Way To Apply For Cover?

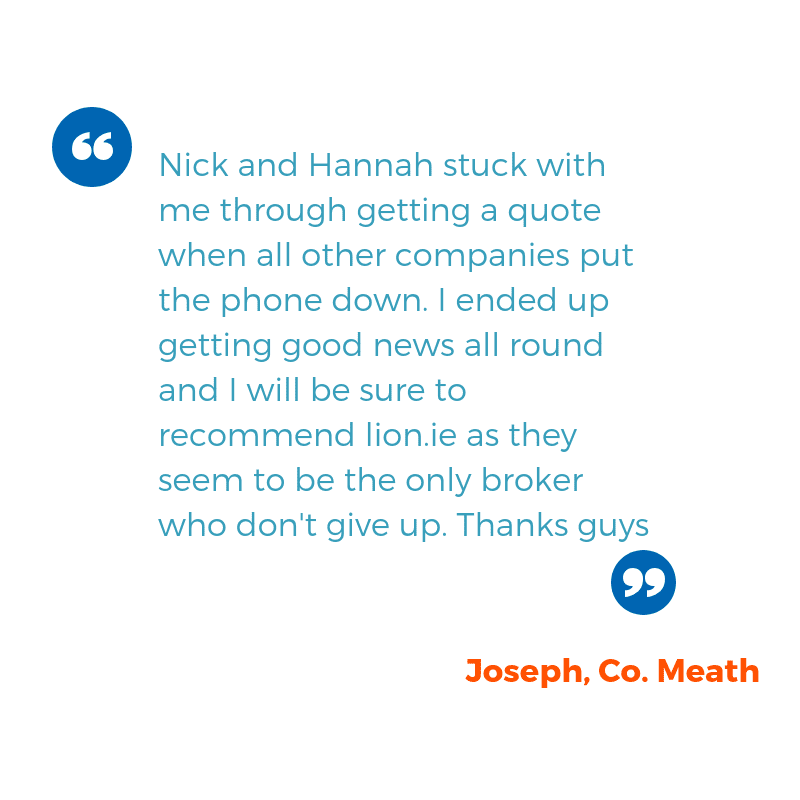

First things first, contact a specialist life insurance broker who knows what they’re doing and can steer you in the right direction.

Do not apply through your bank.

Do not apply directly to an insurance company.

They are both more likely to decline your application.

You’ll have to fess up about the previous decline in all subsequent applications.

Underwriters are already uber-cautious regarding cardiomyopathy, so it’s best to apply with a clean slate.

If you’d like me to help, please complete this questionnaire.

If I can find an insurer wiling to consider an application, they’ll write to your GP for a life insurance medical report.

4. What Information Will the Insurer Need?

HCM is diagnosed based on medical history (your symptoms and family history), a physical exam, and echocardiogram results.

The full gamut of tests include

bloods,

ECG,

chest X-ray,

exercise stress test,

cardiac catheterisation,

CT scan,

and MRI.

The echocardiogram is the most important.

If you have a copy of this, I’ll be able to tell you if it’s worthwhile making a full application or whether the insurers will decline you.

5. Which Insurer is Best?

That’s where I come in.

Before I recommend an insurer, I will speak to all 5, so I know which one is most likely to offer you cover at the best price in the least amount of hassle.

I don’t just apply to the cheapest and hope for the best.

If I don’t think I can get you cover, I won’t waste your time.

6. Will I be Covered for Everything?

Yes, if you get cover, you will be covered for death due to any illness.

The insurer won’t exclude death due to a heart disorder.

7. How long Will it Take?

This depends on your GP.

The insurers are very quick to decide once they have your medical report, but it can take weeks for your GP to complete and return the report.

If you decide to apply through us, we’ll keep an eye on it every step of the way and do all we can to speed the process up.

On average, it takes six weeks from the date we receive the application to the date the insurer makes a decision.

If your GP is on the ball, the process can be quicker.

Give yourself plenty of time.

8. How Much Will it Cost?

It’s another “it depends” answer, I’m afraid.

The two main factors that affect the cost of life insurance with cardiomyopathy are:

Type of cardiomyopathy

Severity of cardiomyopathy

Types of Cardiomyopathy

There are three main types of inherited cardiomyopathy:

Hypertrophic cardiomyopathy (HCM)

Dilated cardiomyopathy (DCM)

Arrhythmogenic right ventricular cardiomyopathy (ARVC)

Another type of cardiomyopathy, Takotsubo cardiomyopathy, can be caused by extreme stress.

This type is not hereditary and often disappears in time.

Other, specialised types of cardiomyopathy include:

Restrictive cardiomyopathy (RCM)

left ventricular noncompaction (LVNC)

Peripartum cardiomyopathy (PPCM).

Severity of Cardiomyopathy

Some people who have cardiomyopathy never have signs or symptoms.

Others don’t have signs or symptoms in the early stages of the disease.

As cardiomyopathy worsens and the heart weakens, signs and symptoms of heart failure usually occur.

These signs and symptoms include:

Shortness of breath or trouble breathing, especially with physical exertion

Fatigue (tiredness)

Swelling in the ankles, feet, legs, abdomen, and veins in the neck

Other signs and symptoms may include dizziness, light-headedness; fainting during physical activity; arrhythmias (irregular heartbeats); chest pain, especially after physical exertion or heavy meals; and heart murmurs. (Heart murmurs are extra or unusual sounds heard during a heartbeat.)

At best, with mild, asymptomatic hypertrophic cardiomyopathy your premium will be double what someone in perfect health will pay.

If you’re showing symptoms of cardiomyopathy, then it’s like to be a decline.

Next Steps

It’s tricky but not impossible to get life insurance with cardiomyopathy as long as you apply to the most sympathetic insurer.

If you’d like some help choosing the best insurer for you, please get in touch by completing this questionnaire or if you prefer, you can schedule a call here

Thanks for reading

Nick

Editor’s Note | We published this blog in 2017 and have updated it since.

Nick McGowan

lion.ie | making life insurance easier