First Time Buyer Mortgage Protection Insurance Ireland 2023

First Time Buyer Mortgage Protection Insurance Ireland 2023 – FAQs

I hear you’re buying your first home – how exciting – congratulations!

And you’re looking for the best deal on mortgage protection insurance, amirite?

But it’s all so confusing:

What’s the difference between mortgage protection and life insurance?

What’s dual life cover??

What the hell is a conversion option???

Which company is the best????

Don’t worry; I’ve got your back.

I know how stressful buying a house is, so I’m here to make the mortgage protection part a doddle.

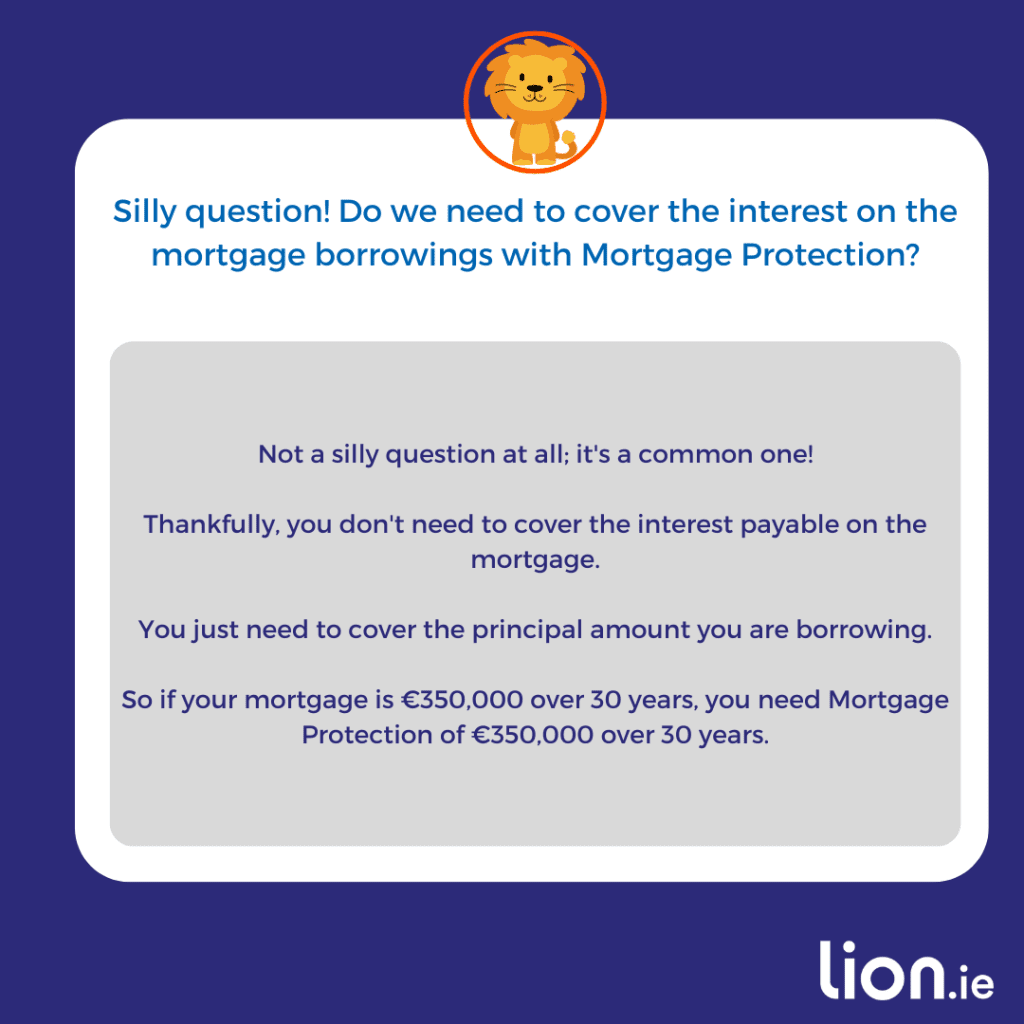

What is Mortgage Protection?

Mortgage protection is a life insurance policy that pays off your mortgage should you die before you pay it off.

It’s mandatory, but the bank, at their discretion, may waive the need for mortgage protection in the following circumstances.

Investment/rental mortgages.

If you can’t get cover due to health reasons, or you can get coverage but only at an outrageous premium.

If you’re over 50 at the time the loan is approved

Consumer Credit Act of 1995

What’s the Difference between Mortgage Protection and Life Insurance?

Mortgage Protection (or mortgage life assurance)

Remember, Mortgage Protection clears your debt to the bank. In other words, it covers the bank’s arse if you die – that’s why they insist you take it out.

Over time, the amount of cover on a mortgage protection policy reduces.

Say you’re getting a mortgage for €250,000 over 25 years.

You die next year with €248,000 outstanding – your policy pays €248,000 to your bank.

You die in 24 years with €600 left to pay – your policy pays €600 to your bank.

Mortgage protection will never leave money to your partner or children.

If you have children, you should also consider a life insurance policy to protect them from financial hardship.

Life Insurance

The cover on a life insurance policy is fixed.

Using our previous example of a mortgage for €250,000 over 25 years.

You die next year with €248,000 remaining – a life insurance policy pays €248,000 to your bank, and €2,000 is left to your family.

You die in 24 years with €600 left to pay – a life insurance policy pays €600 to your bank and the balance to your family.

Some people buy a life insurance policy to clear the mortgage and leave a lump sum for their family.

Don’t do it (or at least read this article first)

As you can see from the above example, if you die early in the policy, your family will be in trouble because they will only get the remaining balance on the policy after it clears your mortgage.

How long could they survive on that?

Top Tip

If you have a mortgage and kids or a partner who depends on you financially, you need a mortgage protection policy and a separate life insurance policy.

Tell me more about Income Protection for First-Time Buyers.

Income protection is the most important type of life insurance policy that you’ve probably never heard of.

If you can’t work for over four weeks due to any illness, income protection will pay you up to 75% of your income until you get back to work or until your policy ends.

Income protection is the foundation of a solid financial plan.

Without it, you’re building your financial plan on sand.

Your income pays for everything.

If your sick pay through work only pays you for a few weeks or you don’t have sick pay, then you need income protection.

It’s that simple.

Want to learn more – here’s our FAQ – a must read.

What about Serious Illness Cover?

Serious illness cover is an additional type of cover that will pay out a tax-free lump sum if you’re struck down with an awful illness (cancer, heart attack, stroke and 54 others), letting you focus on getting better without worrying about how to pay the mortgage.

We prefer income protection but if you have certain health conditions, you may not be able to get income protection so serious illness provides a useful alternative form of protection.

Serious illness cover v Income Protection

Top Tip

Always buy serious illness cover on a separate policy. If you add it to your mortgage protection policy, the bank will get the proceeds on any claim.

Read more about serious illness cover for your mortgage

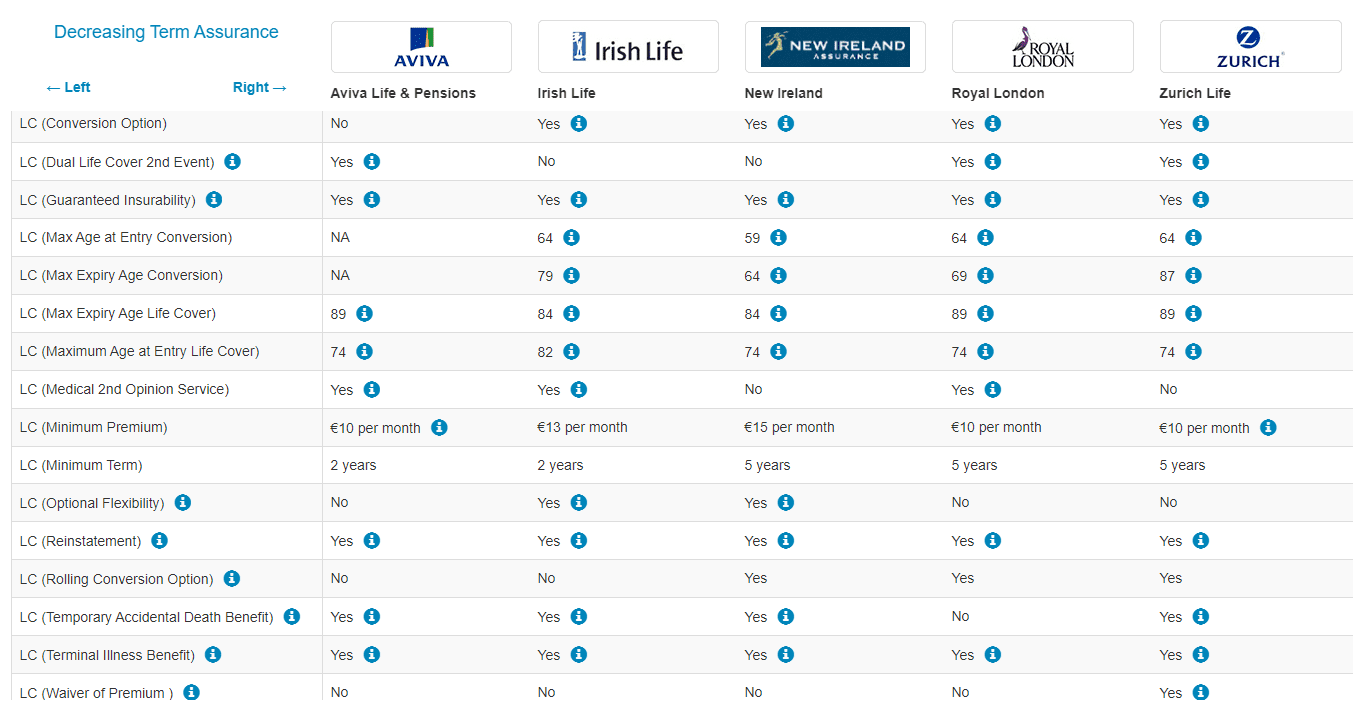

Which company is best for a First-Time Buyer of Mortgage Protection?

Have a butcher’s at our mortgage protection comparison link below.

How much does mortgage protection insurance cost in Ireland?

There are a few factors the insurers have to take into account when calculating how much you will pay for mortgage protection.

follow us on insta

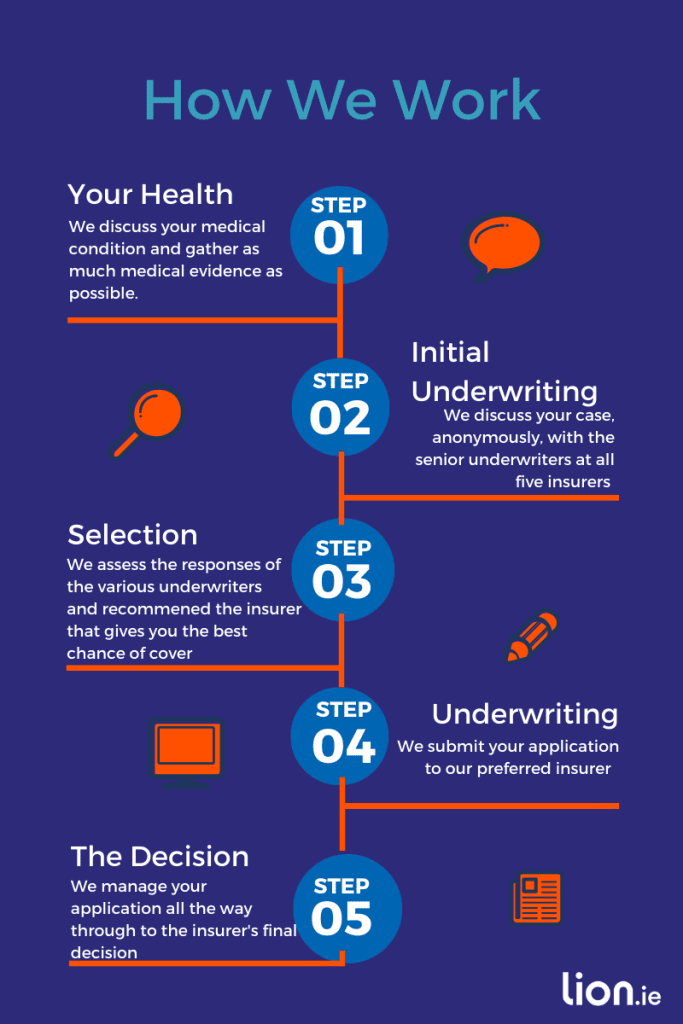

How to get the Best Mortgage Protection Quote?

I knew you would ask that…so I covered it in detail here.

The best mortgage protection quotes are available through a broker, not your bank.

And unlike going to your bank, we can offer quotes from 5 insurers, your bank is tied to one insurer (usually Irish Life).

We offer discounted quotes and straight-talking advice on policies from:

Where can I Compare Mortgage Protection Policies?

Our mortgage protection comparison table makes it easy to compare the various policies on offer at a glance:

And here’s an in-depth look at how to compare mortgage protection in Ireland

At what stage should I be Applying for Mortgage Protection?

Generally, the bank will require your policy a couple of weeks before you’re due to draw down your mortgage, so they have time to review the documentation and assign it.

Watch out, though!

Some banks will put the squeeze on you and pressure you into buying a policy even before they give you the loan offer!

This is unfair and used purely to stop you from shopping for a better value policy.

If your bank is asking you to do this, ask them why?

Remember, you don’t owe the bank anything until they hand over the mortgage cheque, so why should you have to pay mortgage protection premiums before then?

I kinda went off on one there, sorry…back to the question, when should you apply?

I discuss this topic in detail here:

When Should You Apply for and Start Your Mortgage Protection Policy?

You should apply as soon as you have a closing date.

If your closing date is away in the future (3 months+), you should hold off applying until six weeks before you are due to close.

Unless you have a health issue.

If you have an underlying condition, apply asap because it could take ages to get cover if your GP isn’t on the ball.

And please make sure you don’t have any open referrals, tests or investigations as these could result in a postponement.

When do My Payments Start if I Apply for a Mortgage Protection Policy Today?

You won’t pay a cent until you have the policy in your hand, but you can apply well in advance without being out of pocket.

Top Tip

Some of our insurers will give you free cover for the first month (you won’t get that at the bank!),

Over to you…

I know how stressful buying a house can be – so many questions and so many wrong answers.

If you think we’d be a good fit, please call me directly on (01) 693 3382 or drop me an email at nick @ lion.ie

Till then…good luck with the house hunt!

You might find this Glossary / Jargon Buster useful.

By the way, if you’d like me to take a look at your current situation and advise what types of cover you should consider, please complete this questionnaire, and I’ll be back over email with a no-obligation recommendation.

Thanks for reading

Nick

This blog was first published in 2017 and has been regularly updated since