Climate Resilient Development Bond (CRD Bond) proposed with ILS design

A new financial structure that can provide community-based climate insurance or risk transfer protection from the capital markets, while incorporating resilience, advanced funding for loss-prevention and mitigation, through an insurance-linked security (ILS) designed structure has been proposed.

Reinsurance broker Guy Carpenter has collaborated with Dr Franziska Arnold-Dwyer from Queen Mary University of London to produce a briefing document on the new climate-focused ILS structure, laying out a vision for a new kind of mechanism for attracting institutional capital to support climate risk insurance, as well as resilience and mitigation.

The goal is to facilitate improved financial resilience and loss prevention for climate change-related weather risks, while promoting increased cooperation between the insurance sector, government, investors, and other stakeholders.

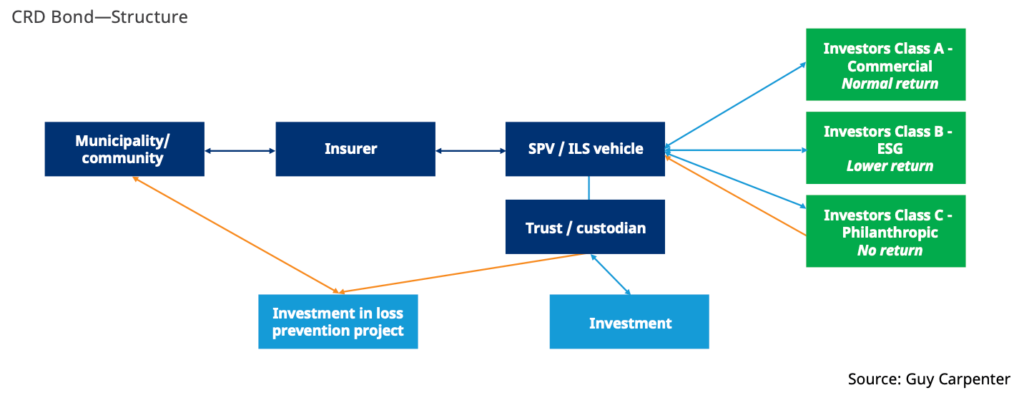

The Climate Resilient Development Bond (CRD Bond) itself brings together community-based insurance capacity provision, a stacked investment approach to bring in differentiated capital with multiple motives, and advanced funding for loss-prevention measures to enhance resilience, all using an enhanced insurance-linked security (ILS) structure that provides protection using a parametric trigger.

It is designed to address large-scale climate-related events for municipalities and the like, enabling insurance, reinsurance and risk transfer protection to be sourced on a multi-year basis, while incorporating a project fund account for a pre-defined and approved project, which is focused on the reduction of exposure to future losses from the specific insured climate-related event.

Overall, the program of insurance or risk transfer is backed by reinsurance capital supplied using an insurance special purpose vehicle (SPV), so a catastrophe bond vehicle or risk transformer, passing the risk to the capital markets through an issuance of bonds or notes.

The investors are envisaged to be of three types, purely commercial, environmental, social and governance focused (ESG), and also philanthropic.

The principal paid will either be purely risk based, or support the project fund component of the structure, depending on the needs and motives of the investors in question.

While the cover is in-force and the structure outstanding, the loss-prevention project implementing, think development of flood defences, or wildfire-resistant housing, is helping to improve the risk profile of the catastrophe bond element, lowering the potential for the structure to be triggered by a loss event.

At the end of the Climate Resilient Development Bond (CRD Bond) term, remaining collateral will be returned to investors (just like catastrophe bonds), but in this case the order of repayment is said to be dependent on the type of investor and their risk and return profile.

A graphic of the proposed structure can be seen below:

“Our contention is that the insurance industry needs a paradigm shift from the traditional post-disaster reaction approach towards an integrated climate risk approach that combines financial protection against the impact of climate-related losses and proactive support with loss- prevention measures,” Guy Carpenter’s briefing paper explains.

Julian Enoizi, Global Head of Public Sector, Guy Carpenter, commented “We need to see a paradigm shift in how the (re)insurance industry addresses climate-related risks. The CRD Bond provides a new type of structure that moves beyond the traditional post-disaster response cover to a truly integrated climate risk approach that combines financial protection against the impact of these perils and proactive support for loss-prevention measures.”

Dr Franziska Arnold-Dwyer, Director of the Insurance, Shipping & Aviation Law Institute at the Centre for Commercial Law Studies, Queen Mary University of London, added, “We believe that the CRD Bond has the potential to make an impactful contribution to the implementation of sustainable and just solutions to the climate crisis. It helps generate financial resilience and loss-prevention capabilities within a mechanism which promotes the principles of equity, sustainable development, and co-operation.”

It’s important to note that this is a very similar concept to the resilience bond that we have covered extensively in the past.

That resilience bond structure first saw the light of day in 2015, and was explored for implementation alongside a number of cities in the past.

The hurdle was in the way the resilience bond tried to connect the resilient infrastructure development with a reduction in risk, which made it very challenging to price and investors failed to get behind the initiative.

That risk reduction, through resilient development efforts, exists in the Climate Resilient Development Bond (CRD Bond) as well.

But, perhaps the market and investor base has moved on sufficiently and the technology has improved to a level that makes that correlation, between the development project steadily enhancing resilience through the life of what is essentially a climate risk or weather peril focused catastrophe bond, and the pricing of the risk changing to account for increased resilience, easier for investors and importantly ILS fund managers to understand, as the existing ILS market will need to be key backers of these structures as well as wider institutional money.

But there is a clear need for this and as we’ve explained in the past, using the resilience bond concept to reduce catastrophe or climate risk while the development of infrastructure for enhancing resilience is ongoing, should appeal to the capital that wants to fund that program of development.

Add in the ESG and philanthropic investment appeal and it’s clear these types of structures should appeal to two categories of investors, making it critical that the commercial (ILS) investors that want to assume and hold the climate or catastrophe risk are comfortable with the way the risk is priced in the first place and the way they are compensated as the resilience is perceived to increase thanks to the development.

Crack that pricing code and the use-cases for this Climate Resilient Development Bond (CRD Bond) could be extensive, making any effort to bring such ILS structures to market extremely important for the ILS market’s own development, as they do present a potentially significant growth opportunity.

Hence, this is excellent to see and we hope the ILS industry engages wholeheartedly and gets behind the development of this structure, or any other, that can transfer climate risk, and reduce it for the future by enhancing climate resilience at the same time.

The parties involved acknowledge the hurdles that must be overcome, saying, “We recognize that the CRD Bond comes with underwriting, modeling, legal and logistical challenges. In fact, we are aware of earlier attempts to launch so-called resilience bonds that could not be modeled to scale the savings associated with the risk reduction to the project costs and the time lag associated with the implementation of an infrastructure project. We think that the scale can be improved by community-based insurance.

“As research into climate-change mitigation and adaptation measures advances, we must also consider local projects that can be identified on science-based evidence and implemented within the terms of the CRD Bond. We also acknowledge that the funding derived from monetizing the risk reduction may not match the full costs of the project. However, it will be a contribution that could make the difference between the project being financially feasible or unaffordable for the relevant community. In addition, we would hope that there is Philanthropic and ESG investor appetite for the CRD Bond as an investment opportunity with clear social and environmental objectives, as well as support from public-private partnerships. As noted above, solutions to the climate crisis and its effects require collaboration at all levels, including from the insurance industry and the financial markets.

“We remain convinced that the insurance industry can rise to the challenge and create a sea change in how its role in addressing the climate crisis is perceived. We consider that the CRD Bond is a sustainable solution to combining financial resilience and loss-prevention measures consistent with the principles of equity, sustainable development, co-operation, and the precautionary principle5 that underpins the Paris Agreement.

“The CRD Bond has the potential to make an impactful contribution from the insurance industry to the implementation of sustainable and just solutions to the climate crisis, as well as heralding a paradigm shift for climate change insurance and beyond by bringing ”loss prevention”’ into focus.”