Average Cost of Private Health Insurance in The UK (2022 Prices)

Before we go any further, we need to state that while our research is thorough, the prices we are sharing are merely indicative. When you get a quote, the price you pay will be different from our findings. There are many reasons for this, from your postcode and age to the level of cover you require. We hope that our research gives you enough of a guide to decide whether you would like to get a comparison quote from a health insurance broker.

What is the average cost of health insurance in the UK?

Based on extensive research, looking at eight leading health insurers (Aviva, Axa, Bupa, Freedom, National Friendly, The Exeter, Vitality, WPA) in 10 UK towns and cities, we can reveal the average cost of health insurance in the UK is £86.07 per month (£1,032.84 per year)*.

*Pricing research conducted in February 2022. Average found by obtaining quotes from 8 leading providers for six ages in ten towns and cities. See later in this post for our full methodology.

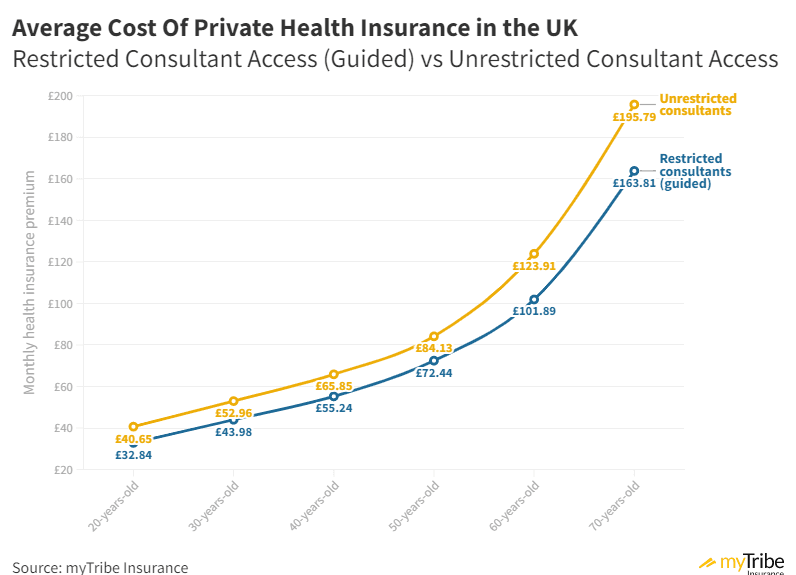

A significant difference between the insurers we sampled is whether they offer “Guided Consultants”, which limits you to a pool of medical practitioners the health insurance companies have preselected. How they’ve preselected them is a bit of a mystery, but one would assume that as having guided consultants reduces the cost of your policy, the medical practitioners have likely have agreed to favourable terms with the insurers. Importantly, all of the providers that offer guided consultants also offer “non-guided” (unrestricted) options, so, for fairness, we’ve included both in our research.

Important note on guided consultants

As outlined, you are restricted to the consultants on your insurer’s “approved” list by going down the guided consultant route. That means that if there is a particular specialist that you want to perform your surgery or provide your care and they aren’t on the list, you can’t use them. We want to highlight this, as health insurance is often marketed as giving you more control over who treats you; however, with guided consultants, you somewhat give up that control. We’re in the process of creating a separate article specifically about this topic and the potential pitfalls, so please watch this space.

Only four of the providers we looked at (Aviva, Axa, Bupa and Vitality) offer “Guided Consultants” (albeit with different names), so prices relating to guided consultants are based on those four providers only.

Click here to download a sharable version of this visualisation for your website. Please credit myTribe Insurance and link to this page as the source when re-publishing our research.

Applicant age

Restricted Consultant Access

Unrestricted Consultant Access

20-years-old

£32.84*

£40.65*

30-years-old

£43.98*

£52.96*

40-years-old

£55.24*

£65.85*

50-years-old

£72.44*

£84.13*

60-years-old

£101.89*

£123.91*

70-years-old

£163.81*

£195.79*

Source: myTribe Insurance

*Average based on quotes from eight leading health insurers in 10 UK cities. We opted for a comprehensive policy, with a £250 excess (or as close as possible), outpatient cover limited to a maximum of £1,500 in claims per year, and we included therapies cover. We defaulted to each provider’s standard hospital list and used moratorium underwriting. Mental health cover, dental, optical and travel cover were all excluded. Prices accurate as of 16th February 2022. Please note these prices are purely illustrative; the cost of your policy will be different.

Aviva, Axa, Bupa and Vitality offer discounts if you opt for “guided consultants”, which gives you less choice over who provides your treatment. Not all insurers offer this, so we opted included both guided and non-guided prices in our research.

Key takeaways

Having unrestricted consultant access (non-guided) will on average increase your premium by 20%.Premiums increase by between 25-33% every ten years, from 20 to 50 years old. However, after that, they increase more sharply with an approximate increase of 44% between 50 and 60 years old, and 59%, between 60 and 70 years old.Prices are nearly 400% higher for a 70-year-old vs a 20-year-old

How much does your postcode affect your health insurance premium?

Most health insurance providers charge different amounts based on where you live in the UK. There are several reasons for this, and how each insurer calculates prices will vary; however, typically, these are some of the factors they take into consideration:

The cost of treatment in private hospitals and clinics close to you.The claim rate of your postcode.How affluent your area is.How many policyholders there are in your area.

As we say, exactly how the insurers calculate this will be unique to them, but it’s important to note that the price you pay will depend on where you live in most cases.

Freedom Health Insurance doesn’t adjust pricing based on where you live.

Freedom Health Insurance is the only insurer we looked at that didn’t adjust their prices based on where you live. Whether you live in London or Edinburgh, the price you pay will be the same.

We asked Freedom Health Insurance why they take a different approach to most.

“We believe that we should be able to explain the premiums we charge to our customers, and establishing a link between a postcode and how much or how often a customer might claim under a medical insurance policy is unclear and difficult to understand. At Freedom, we believe in choice and that rating factors should reflect risk. As yet, we have not been convinced that the use of detailed postcode data in PMI pricing reflects risk in a way we are comfortable with or able to explain.”

“We believe that we should be able to explain the premiums we charge to our customers, and establishing a link between a postcode and how much or how often a customer might claim under a medical insurance policy is unclear and difficult to understand. At Freedom, we believe in choice and that rating factors should reflect risk. As yet, we have not been convinced that the use of detailed postcode data in PMI pricing reflects risk in a way we are comfortable with or able to explain.”

Alistair Sclare – Managing Director

Freedom Health Insurance has one of the most extensive standard hospitals lists of any of the providers we’ve reviewed. However, some expensive hospitals, particularly those located in Central London, won’t be covered as standard, which is consistent with the other providers we’ve researched. You can, however, opt to include those hospitals by taking out their “London Plus” hospital list option.

National Friendly also has less location-based pricing.

While Freedom is the only provider we looked at that doesn’t change prices based on where you live, National Friendly also has less pricing variation than others. Of the ten cities we looked at, the only locations where National Friendly charged more were London and Manchester.

Price of health insurance in key towns and cities

We obtained pricing from the eight leading health insurers in ten towns and cities across the UK. As we explained earlier in this post, we have pricing for both restricted consultant access and unrestricted, however, to keep this part of our research as simple as possible, we’ve opted to take an average of the two, so we can provide you with just one price per age, per location.

Click here to download a sharable version of this visualisation for your website. Please credit myTribe Insurance and link to this page as the source when re-publishing our research.

Where is the cheapest place to buy health insurance in the UK?

Our research found that of the ten towns and cities we looked at, Edinburgh, Scotland was consistently the cheapest place to buy health insurance in the UK, at 15.74% under the national average.

Where is the most expensive place to buy health insurance in the UK?

London is the most expensive place in the UK to buy health insurance at 25.55% above the national average in our research. Manchester is the next most expensive, at 12.60% above the national average.

Ranked list of towns and cities (least to most expensive) vs national average

Edinburgh -15.74%Leeds -7.35%Bristol -6.05%Cardiff -5.95%Oxford -5.35%Cambridge -5.06%Bournemouth +3.00%Birmingham +4.54%Manchester +12.60%London +25.55%

Findings and key takeaways

Edinburgh was consistently the cheapest place to get health insurance, at 15.74% under the national average overall.London was consistently the most expensive place to get health insurance, at 25.55% above the national average overall.Birmingham, Manchester and Bournemouth were all above the national average.Cambridge and Bristol are almost the same as the national average.Oxford, Leeds and Cardiff are all less than the national average for every age.

How do health insurers compare on price?

Comparing health insurers with each other is pretty tricky because all of their policies have differences that impact their prices. In this next section, we’ve looked to do as fair a comparison as possible, highlighting key differences where we think it’s appropriate.

We strongly recommend that you speak to an independent health insurance broker to receive a personalised comparison quote and individual advice.

Unrestricted consultant access (non-guided)

All of the health insurance providers we sampled have the option of unrestricted consultant access, and therefore, we’ve decided to share those results with you first.

Please note: Opting for “Guided Consultants” is usually around 20% cheaper than unrestricted access if you are interested in how the four providers that offer this option compare, please see the next section of this article.

Key findings

Vitality was the cheapest provider in 5 of 6 ages sampled; however, a unique 10% discount was applied on the basis, the applicant hadn’t had any significant health issues in the past three years (no other provider offers this). Even by removing that 10% discount, Vitality is still among the cheapest insurers for most ages.The Exeter and WPA are both competitive through all ages, with neither ever being the cheapest nor the most expensive.Aviva was the most expensive provider for every age, barring for 20-year-olds.Bupa starts well but loses competitiveness as age increases.Axa starts well but loses competitiveness as age increases.Freedom was relatively competitive up until 50-years-old, after which their prices were above average.National Friendly is expensive if you’re young but improves in competitiveness as age increases and is the cheapest provider for 70-year-olds.

Restricted Consultant Access (guided)

Only four of the eight providers we looked at allow you to reduce your premium by restricting your access to their pool of pre-selected medical practitioners. Those insurers are Aviva, Axa, Bupa and Vitality – here’s how they compare.

Key findings

Aviva was consistently the most expensive provider, the highest in 5 out of 6 ages.Vitality was cheapest at every age from 40 upwards (4 out of 6); however, a 10% discount was applied based on the applicant having no significant medical issues in the past three years. By removing that discount, Vitality was still among the cheapest providers.Axa starts very competitively, coming in as cheapest for 20-year-olds; however, as age increases, their competitiveness reduces.Bupa is competitive for 20 and 30-year-olds; however, beyond that, their competitiveness reduces.

Our research methodology

Private health insurance is a complicated financial product that can be configured in many ways – because of that, getting a meaningful average is difficult. While all insurers offer slightly different products, we’ve done our best to minimise the variables to provide you with some guide prices.

Our data sample

For this research, we focused on the cost of an individual policy, with the applicant being one of the following ages, 20, 30, 40, 50, 60 or 70 years old.

For each of those ages, we got quotations in 10 cities around the UK: Birmingham, Bournemouth, Bristol, Cambridge, Cardiff, Edinburgh, Leeds, London, Manchester, and Oxford.

Finally, we received quotes from the eight best private health insurance providers, WPA, The Exeter, AXA Health, Freedom, Bupa, National Friendly, Vitality and Aviva for those ages in those cities.

Policy configuration

To get quotes from each of the eight insurers, we needed to decide what level of cover our fictional applicant required. Working with external health insurance brokers, we built a list of policy requirements based on what a typical policy might look like; in short, these were:

The policy was comprehensive, scoring a four or five-star Defaqto rating.We included Outpatient Cover, limited to a maximum of £1,500 a year.We included Therapies Cover (i.e. physiotherapy, acupuncture and homoeopathy).The policy excess was set at £250 (or as close to that as possible)We excluded Mental Health Cover (Bupa, however, include this as standard).We defaulted to the insurer’s standard hospital list.We excluded Dental, Optical and Travel Cover.The policy was underwritten on a moratorium basis.We got prices for both guided consultants and their non-guided options.

Data sources:

Aviva Website (February 2022)

Axa Website (February 2022)

Bupa Website (February 2022)

Freedom Website (February 2022)

National Friendly Website (February 2022)

The Exeter Website (February 2022)

Vitality Website (February 2022)

WPA Website (February 2022)

All prices accurate as of 16th February 2022.

Closing thoughts

We hope you find this information useful; if you have any questions or would like full access to our research, please let us know by emailing contact@mytribeinsurance.co.uk.

As a final reminder, please take the information provided on this page as a guide only. While our research has been extensive, you’re always best to speak to a health insurance broker who can perform a detailed market review on your behalf. To request a free comparison quote from one of our recommended brokers, please click the button below.

What is the average cost of health insurance for a 20-year-old?

Based on extensive pricing research conducted in April 2022, we found that the average cost of private health insurance for a 20-year-old is £36.75 per month.

What is the average cost of health insurance for a 30-year-old?

Based on extensive pricing research conducted in April 2022, we found that the average cost of private health insurance for a 30-year-old is £48.47 per month.

What is the average cost of health insurance for a 40-year-old?

Based on extensive pricing research conducted in April 2022, we found that the average cost of private health insurance for a 40-year-old is £60.55 per month.

What is the average cost of health insurance for a 50-year-old?

Based on extensive pricing research conducted in April 2022, we found that the average cost of private health insurance for a 50-year-old is £78.29 per month.

What is the average cost of health insurance for a 60-year-old?

Based on extensive pricing research conducted in April 2022, we found that the average cost of private health insurance for a 60-year-old is £112.90 per month.

What is the average cost of health insurance for a 70-year-old?

Based on extensive pricing research conducted in April 2022, we found that the average cost of private health insurance for a 70-year-old is £112.90 per month.

Which private health insurance provider is the cheapest?

Vitality is the cheapest private health insurer in the UK, with their policies costing on average £71.80* per month, 18% below average

*The quotes we received from Vitality included a 10% discount on the basis the applicant hadn’t suffered from any substantial medical concerns in the previous three years; Vitality is the only provider to offer this type of discount. Vitality is still very competitive by removing that discount (10% under the average). Importantly, they aren’t always the cheapest for every age in every location, so please consult with your health insurance broker before making any decisions.

Which private health insurance provider is the most expensive?

Aviva is the most expensive private health insurer in the UK, with an average policy cost of £106.89 per month, 23% above average.

Importantly, expensive doesn’t always mean best. When we reviewed Aviva earlier in the year, they came out at the bottom of eight top providers for policy comprehensiveness and customer service.

Is private healthcare expensive in the UK?

Whether private healthcare is expensive or not is difficult to answer. It gives many benefits, but they do come at a cost. The average price of a private healthcare policy in the UK is £1,032.84 per year (April 2022); however, you could pay considerably less or more depending on your age and the level of cover you require. For example, a 30-year-old would pay on average £581.64 per year, and a 60-year-old £1,354.80.

What’s the monthly cost of health insurance in the UK?

On average, a health insurance policy in the UK costs £86.07 per month (accurate as of April 2022). However, this average is based on people between 20 and 70 years old. If you are under 50, your policy will likely be less than the average.

Have questions or like to speak to someone about our research? Please email contact@mytribeinsurance.co.uk.