Homeowners Claims Costs Rose Faster Than Inflation for 2 Decades

By Max Dorfman, Research Writer, Triple-I

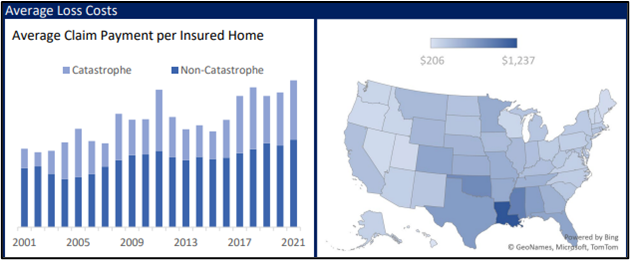

The cost of claims per insured home in the United States has increased at a rate outpacing inflation over the past 20 years, according the Insurance Research Council (IRC) — like Triple-I, an affiliate of The Institutes.

A new IRC study, Trends in Homeowners Insurance Claims: 2001–2021, attributes this to a combination of natural catastrophes, human-made disasters, rising home-repair costs, and ongoing population migration into disaster-prone areas.

Insurers also continue to wrestle with insurance fraud and claim abuse following disastrous events. These trends have cut into profits and led several major insurers to reduce their capacity in some U.S. states or leave the homeowners market entirely.

Other findings include:

Countrywide average loss costs (average claim payment per insured home) increased throughout the past two decades and rose nine percent in 2021.Claim severity is increasing, while frequency is declining—in part because of widespread adoption of higher policyholder deductibles, including percentage deductibles for specified perils, and premium surcharge programs designed to reduce the number of lower-cost claims.Catastrophe losses play an increasing role because of natural disaster trends and the methods used to define and categorize catastrophe claims.Average loss costs for claims vary widely by state. States with the highest loss costs are Louisiana and Mississippi; states with the lowest are Hawaii and Maine.States with the highest claim frequency over the period include Louisiana, Mississippi, and Oklahoma. States with the highest severity include California, Alaska, and Florida.

“During the two decades of the study period, the U.S. homeowners market has experienced a surge in volatility, mainly driven by a barrage of disasters, such as hurricanes Katrina, Ike, Michael, Rita, Sandy and Wilma and California fires,” said Dale Porfilio, IRC president and chief insurance officer for Triple-I.

Porfilio also noted that another challenge facing the homeowners insurance market is the continued threat of insurance fraud and claim abuse, especially after natural disasters.

“Industry and government organizations have increased efforts to inform consumers about potential scams, to investigate and prosecute the perpetrators, and to enact legislative changes to make systems less vulnerable to abuse,” Porfilio added.

Learn More:

How Inflation Affects P/C Insurance Rates and How It Doesn’t (Triple-I Issues Brief)

Drivers of Homeowners’ Insurance Rate Increases (Triple-I Issues Brief)

Florida’s Homeowners Insurance Crisis (Triple-I Issues Brief)

Louisiana Insurance Crisis (Triple-I Issues Brief)

From the Triple-I Blog

As Building Costs Grow, Consider Your Homeowners’ Coverage

Lightning Sparks More Than $1 Billion in Homeowners Claims Over Five Years

Triple-I Brief Explains Rising Homeowners’ Insurance Premium Rates

Homeowners Premiums Rise Faster Than Inflation; Expect This to Continue