What is a mortgage escrow account and how does it work?

It’s an exciting time for you- after months of house shopping, you’ve found the home of your dreams. And being your very first home purchase, you’re super excited. But during your conversation with your mortgage lender, the term “mortgage escrow account” keeps being thrown around and you don’t understand what it means. This post explains a mortgage escrow account, and provides some examples so you know what it is and how it works.

What is a mortgage escrow account?

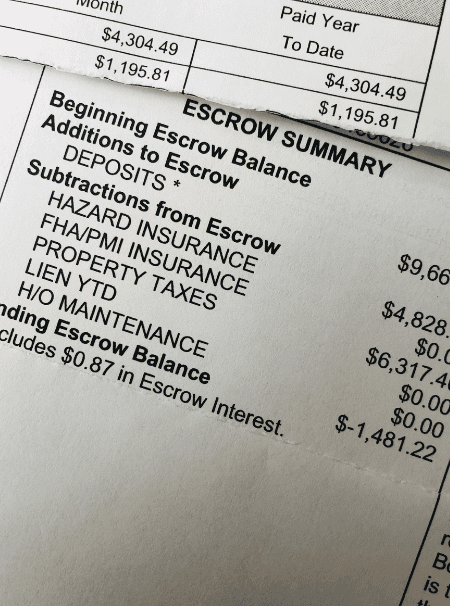

In simplest terms, it is an account set up through your lender to make payments for property taxes and Ohio homeowners insurance. To help you better understand how it works, two examples are shown below, the first showing how the mortgage escrow account works when you first buy your house and the second after the first year of home ownership.

How does the mortgage escrow account work when you first buy your home?

Your insurance agent and you work together to determine the coverage needed for your homeowners insurance policy.When you and your agent finalize the homeowners insurance quote, the agent will communicate the annual premium to the mortgage lender.Let’s say the annual premium is $600. Your mortgage lender divides the $600 by 12 (an Ohio homeowners insurance policy is a 12 month policy), which equals $50.If you’re also paying property taxes via escrow, the annual property tax would also be divided by 12. When you elect to do an escrow account, your monthly mortgage payment includes the loan principal and interest PLUS the monthly homeowners insurance premium (in this example $50) and 1/12 of the property tax. This allows the account to build over 12 months so when the homeowners insurance invoice is sent, the money is in the account to pay it.

*Note– when you first buy your house, you will be required to pay the annual premium in full either before closing or at the closing. Why? Because there’s no account yet built up to draw from. Insurance is always paid in advance. So if your closing date is September 1, 2021, you will owe the premium from September 1, 2021- September 1, 2022.

The monthly mortgage payment that will be collected over the following 12 months will pay September 1, 2023- September 1, 2024. Again, homeowners insurance is paid in advance, so the funds need to be in the account to pay when that invoice arrives. Which leads us to the next example.

How does the mortgage escrow account work after your first year of ownership?

Let’s say the homeowners insurance renewal is $600 again. The insurance company sends the invoice to the mortgage lender in advance of the renewal date (usually about 30 days)The mortgage lender sends the check to the insurance company.

Please note- in the years following your home purchase, it’s likely your mortgage escrow payment will change, and most likely increase. Read Why Did My Mortgage Escrow Payment Increase for the most common examples.